STENOCARE published on August 21st the company’s Q2-report for 2024. The following are some key points that we have chosen to highlight in connection with the report:

- Financial development during the period

- Launch of premium products ahead of plan

- Financial position and burn rate

Sales Lower than Expected due to Unfavourable Market Dynamics Concerning Pricing and Reimbursement Principles

STENOCARE’s net sales amounted to DKK 0.7m (1.7), corresponding to a decrease of 57% compared to Q2-23, which was below Analyst Group’s expectations. The lower than anticipated sales are, among other things, a result of a decrease in product prices and increased competition due to higher product price subsidy in Denmark, as well as slower sales in international markets. STENOCARE had several growth drivers going into 2024, including the balanced oil approved in Denmark, a new product in Australia and entering the German market, which has not delivered growth as expected, even though the company has successfully made the planned strategic progress in these countries. This is anticipated to be due to the integration of medical cannabis into clinical practice has not progressed as rapidly as was anticipated a few years ago.

Based on the financial performance and the outlook for 2024 STENOCARE announced on August 20th that the company updates the guidance for 2024, from gross sales of DKK 12-18m to DKK 6-8m and that the expected break even at the end of 2024 is no longer realistic. The revised guidance is primarily based on the earlier mentioned increasing competition and the dynamic pricing model in Denmark, which has entailed a decline in prices and hence affected STENOCARE’s net sales, even though the company expects to deliver +20% more products units in Denmark during 2024. Even though sales are expected to improve in H2-24 compared to H1-24 we are likely to update our financial forecasts for STENOCARE based on the financial performance in Q2-24 as well as the updated guidance.

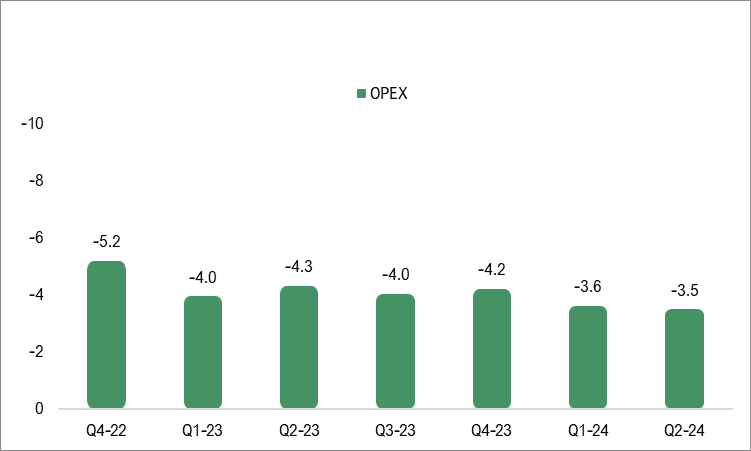

The Cost Base Continues to Decrease

The operational expenses, excluding depreciation, amounted to DKK -3.5m (-4,3), corresponding to a decrease of 19%. Thus, we believe that STENOCARE is continuing to optimize its cost structure to reduce the company’s burn rate, given the lack of sales acceleration so far, which we view positively.

Launch of Premium Products Ahead of Plan

During Q2-24, STENOCARE announced that the company’s premium product, the Astrum oil, is ready for launch on the Australian market. The product is expected to have several benefits compared to the medical cannabis oil available today, including a higher, more uniform, and faster uptake in the blood. With this launch, we see STENOCARE as a first mover in next generation medical cannabis oil products, why we see that the company can gain an advantage against potential competitors. After the end of the period, on July 31st, STENOCARE announced that the Astrum oil has been approved in Europe’s largest medical cannabis market, Germany.

Moreover, STENOCARE also announced that the company is looking into an expansion to Canada. The Canadian market is a vast market with a lot of competition but with STENOCARE’s premium product Astrum, Analyst Group believes that STENOCARE can position the company’s products within a distinct niche, even in the most competitive markets such as the Canadian, because of the unique benefits with the products patented oil technology. This enables STENOCARE to become one of the few European companies capable of capitalizing on one of the largest medical cannabis markets globally.

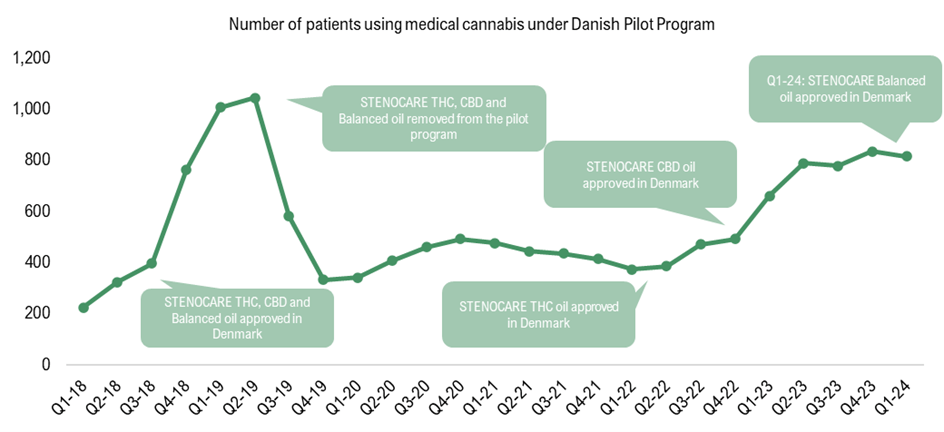

Stable Patient Development in Denmark

The number of patients using medical cannabis under the Danish pilot program had a stable development in Q1-24, which is the last published figures, amounting to 816 compared to 662 in Q1-23. When looking at the number of patients using medical cannabis under the Danish pilot program, the number of patients has historically increased after new products from STENOCARE has been approved as illustrated in the graph below. From April 18th, STENOCARE’s balanced oil has been approved for sales in Denmark, which historically has represented +50% of the total sales, why we estimate that the newly approved balanced oil will accelerate patient growth in the coming quarters, which is also expected to drive sales volume. However, due to price declines the total sales is expected to be lower than earlier anticipated in the coming quarters.

Capital Increases and Reduction of Debt but Additional Funding Expected to be Needed

During Q2-24, STENOCARE strengthened the cash position through warrants of series TO2 with net proceeds of approximately DKK 4.2m and a directed issue of DKK 1m to the major shareholder HHTM ApS. Moreover, STENOCARE negotiated a loan agreement with shareholder HHTM ApS amounting to DKK 2.8m with a slightly better interest rate than the existing debt (1.97% vs 2%) and with a loan term of 30 months compared to the existing debt of DKK 6m which was due on January 1st, 2025. Through the new loan, the directed issue and partial of the new proceeds from TO2 warrants, the existing debt of DKK 6m was repaid, leading to the total debt on STENOCARE’s balance sheet amounting DKK 2.8m after the transactions.

Through these activities, STENOCARE’s debt has decreased, and the cash position has strengthened, which we view positively. The transactions are not visible in the Q2-report as they were completed just after the end of the quarter. Given that the “old” debt of DKK 6m has been repaid with the new loan of DKK 2.8m, the proceeds from the directed issue of DKK 1m, we estimate that approximately DKK 2.2m of the proceeds from TO2 has been used to repay the loan, which leaves approximately DKK 2m as cash at bank at the end of Q2-24. The burn rate in Q2-24 was DKK -0.77m per month and given the financial performance in H1-24, the updated guidance, and the estimated cash balance of approximately DKK 2m at the end of Q2-24, Analyst Group believes that the company will need to secure additional funding, most likely through a capital raise.

To summarize, STENOCARE delivered a report with lower sales than estimated but also lower costs than expected. We continue to see several growth drivers, even though they are materializing more slowly than we previously anticipated, however we expect higher revenue in H2-24 compared to H1-24.

We will return with an updated equity research report of STENOCARE.