STENOCARE, founded in 2017, is a Danish pharmaceutical company who became the first company to receive permission to import, distribute as well as to cultivate and produce medical cannabis in Denmark in 2018. Today, STENOCARE sources its products from several international suppliers and distribute these to a growing number of international markets. The Company also has their own indoor cultivation facility in Denmark, which is strategically focused on meeting pharmaceutical standards. STENOCARE was listed on Spotlight Stock Market on October 26th, 2018 and is today listed on Nasdaq First North Growth Market Denmark since May 15th, 2020.

Press releases

All Focus on Astrum

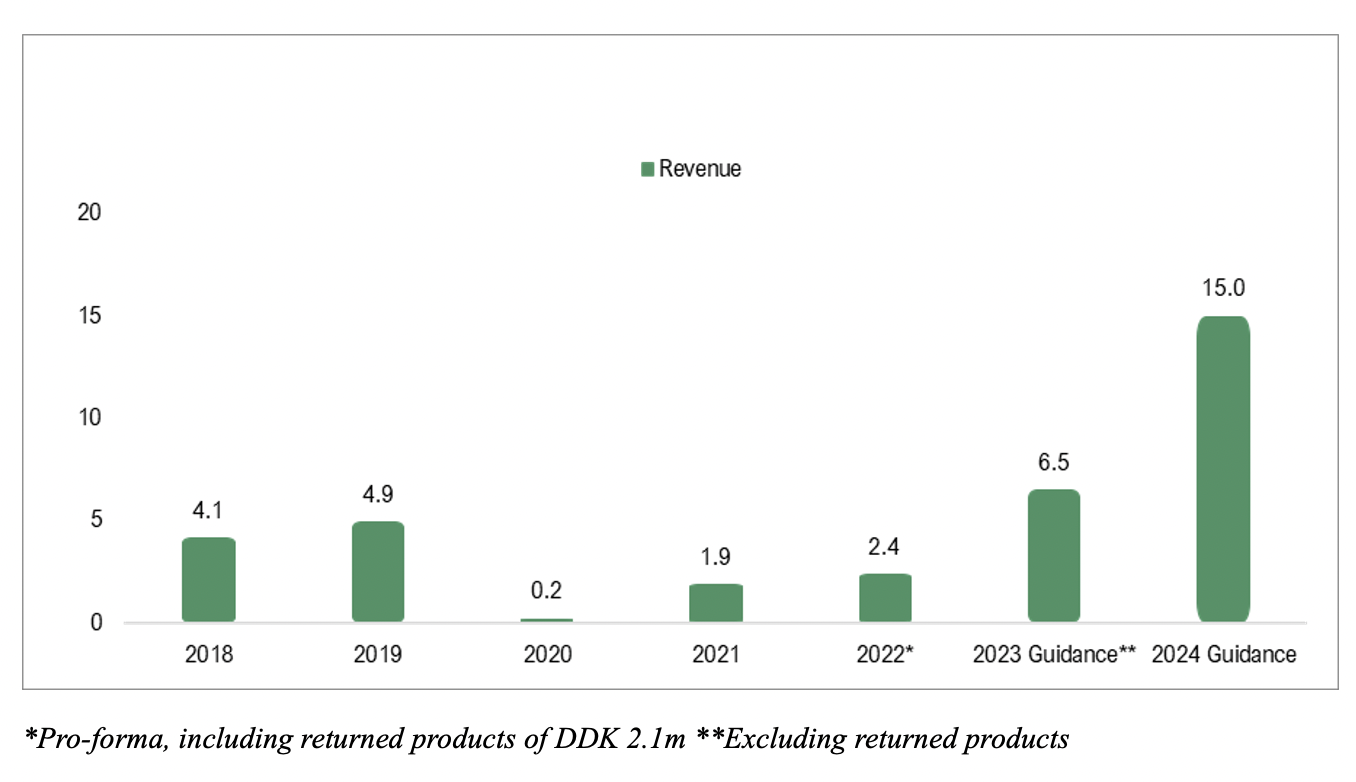

STENOCARE A/S (“STENOCARE” or the “Company”) is a medical cannabis trading company with products approved and available for patients in six countries. The Company has recently launched a premium product, Astrum oil, which Analyst Group sees as an important growth driver in the coming year, as it distinguishes STENOCARE from competitors, providing improved, uniform and faster uptake in the blood. The product became available to patients in three countries during 2025, Germany, Australia, and Norway. With estimated net sales of DKK 14.9m by 2027, an applied P/S multiple of 2.5x and a discount rate of 16%, a potential present value per share of DKK 0.64 (1.3) is derived in a Base scenario.

- Net Sales Amounted to DKK 1.3m in Q4-24

STENOCARE reported net sales of DKK 1.3m (1.3) in Q4-24, 21% above Analyst Groups estimate of DKK 1m. The Company continued to experience increased competition and a special situation in Denmark with a competing magistral product being supported with 85% patient subsidy from the Danish Medicines Agency. If the situation is solved during 2025, we see this, in combination with start of sales of the innovative Astrum oil as important sales growth drivers in the upcoming year.

- Additional Cost Savings Expected from Updated Strategy

The new STENOCARE 3.0 strategy states that the Company will focus on trading prescription-based medical cannabis and exit the production activities at STENOCARE’s own indoor cultivation facility. Hence, the Company is expected to be relieved of all related costs, including the significant long-term lease and equipment lease. This represents a financial obligation of approximately DKK 14m over the next six years and additional DKK 5m in annual operational costs. Through this updated strategy we estimate a decreasing cost base in 2025 and a shorter way to profitability, expected on an EBITDA level in 2027.

- The Financial Position Strengthened

STENOCARE’s cash balance at the end of Q4-24 amounted to DKK 1.4m and has been strengthened with estimated net proceeds amounting to DKK 7.9m from a rights issue in January. Based on an estimated decreasing cost base and growing net sales, we estimate that STENOCARE are financed for the remainder of 2025.

- Updated Valuation Range

We have updated our valuation scenario following the rights issue which meant an increased number of shares, thus dilution, however partly offset by a lower discount rate through a lower financial risk. Moreover, the exit from the Company’s cultivation activities has affected the long-term financial outlook as sales from the own cultivation facility had higher estimated margins. However, it enables a shorter path to positive results through cost savings in the coming years. Nevertheless, the updated forecast impacts our valuation range.

6

Value drives

2

Historical profitability

7

Management & Board of Directors

8

Risk profile

All analyses of companies from 2020 onwards are rated based on a new rating system - Value Driver, Historical Profitability and Management & Board ranges from 1 to 10, where 10 is the highest rating. The risk profile ranges from 1 to 10, where 10 is to be considered the highest risk. Stock analyses of companies published before 2020 have been rated based on a different model.

Tough Market Conditions Hampers the Growth

STENOCARE A/S (“STENOCARE” or the “Company”) continues to experience tough market conditions in Denmark because of increased competition and higher subsidy from the Danish Medicines Agency on a competing product, which has affected sales. Moreover, sales in international markets has been slower than earlier expected, due to a more sluggish market. However, we still see growth opportunities in the coming years, primarily through STENOCARE’s new innovative premium product, Astrum oil. Nevertheless, the current market conditions has led us to update our financial forecasts of STENOCARE and with estimated net sales of DKK 15.6m by 2026, and with an applied P/S multiple of 2.5x, a potential present value per share of DKK 1.3 (4.0) is derived in a Base scenario. The updated valuation is a result of the updated forecasts as well as the increased financial risk.

- Gross Sales Amounted to DKK 1.1m in Q3-24

STENOCARE reported gross sales of DKK 1.1m (2.4) in Q3-24, corresponding to a decrease of 53%. Due to returns of expired products amounting to DKK 2m, as a result of lower demand than expected leading to expired products, net sales amounted to DKK -0.9m (0.2). The Company are experiencing increased competition and a special situation in Denmark with a competing magistral product being supported with 85% patient subsidy from the Danish Medicines Agency. We expect the challenges to remain throughout 2024 but see opportunities for growth in the long term, primarily through a successful launch of the Astrum oil.

- Operates With a Lean Organization

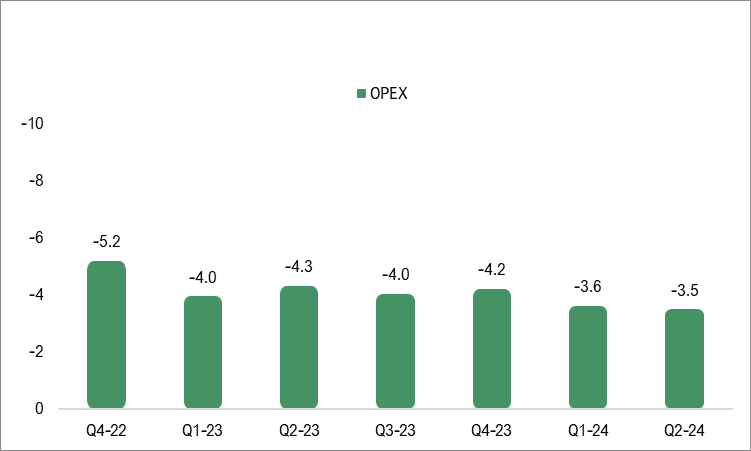

The operational expenses, excluding depreciation, amounted to DKK -3m (-4), corresponding to a decrease of 26%. Thus, we believe that STENOCARE is continuing to optimize the cost structure to reduce the Company’s burn rate, given the lack of sales acceleration so far, which we view positively on.

- Additional Funding Needed

STENOCARE’s cash balance at the end of Q3-24 amounted to DKK 0.1m and given that the Company are yet to show a positive cash flow, STENOCARE will need additional funding to keep the operations going and to leverage future growth opportunities. We assess that a capital raise through a new share issue is the most likely scenario, which, however, may occur under less favorable terms for existing shareholders given the recent weak share price performance.

- Updated Valuation Range

Considering the results during the first nine months of 2024 and the current tough market conditions both in Denmark, because of increased competition higher subsidy on a competing product, as well as in international markets, we have updated our financial forecasts. Given the updated forecasts, with lower growth and profitability, as well as a high financial risk, we have updated our valuation range in all scenarios.

6

Value drives

2

Historical profitability

7

Management & Board of Directors

8

Risk profile

All analyses of companies from 2020 onwards are rated based on a new rating system - Value Driver, Historical Profitability and Management & Board ranges from 1 to 10, where 10 is the highest rating. The risk profile ranges from 1 to 10, where 10 is to be considered the highest risk. Stock analyses of companies published before 2020 have been rated based on a different model.

Delivers on Key Strategic Initiatives

STENOCARE A/S (“STENOCARE” or the “Company”) has executed on several strategically important milestones during H1-24, including approval of the balanced oil in Denmark and the launch of premium products in Australia and Germany. However, higher product price subsidy has increased competition from Magistrel products in Denmark, and the market growth has been slower than expected which has affected sales. This has led us to update our financial forecasts for STENOCARE and with estimated net sales of DKK 30.2m by 2026, and with an applied P/S multiple of 4x, a potential present value per share of DKK 4.0 (8.8) is derived in a Base scenario. The updated valuation is a result of the updated forecasts, a multiple contraction in the industry as well as an increase in shares outstanding from capital raises.

- Net Sales Amounted to DKK 0.7m in Q2-24

STENOCARE reported net sales of DKK 0.7m (1.7) in Q2-24, corresponding to a decrease of 57% Y-Y. Unfavorable market dynamics has impacted STENOCARE’s sales negatively where higher product price subsidy in Denmark has increased competition and resulted in price decreases. Moreover, sales in international markets have been slower than estimated as the integration of medical cannabis into the health care industry has been slower than estimated. However, STENOCARE has successfully made the planned strategic progress in several markets, which has laid the ground for future growth. Nevertheless, considering the current market conditions, we have updated our sales forecast downwards in this update.

- Operates With a Lean Organization

The operational expenses, excluding depreciation, amounted to DKK -3.5m (-4,3), corresponding to a decrease of 19%. Thus, we believe that STENOCARE is continuing to optimize the cost structure to reduce the Company’s burn rate, given the lack of sales acceleration so far, which we view positively.

- Launch of Next Generation Products

During Q2-24, STENOCARE announced the launch of the Company’s premium product, Astrum oil, which is expected to be available for patients in Australia and Germany from Q4-24. The Astrum oil offers several benefits which the industry have struggled with historically, including a higher, more uniform, and faster uptake in the blood. Analyst Group believes that the Astrum oil has the potential to revolutionize the industry and is expected to be an important sales driver from 2025.

- Updated Valuation Range

Considering the results in H1-24 and the current more unfavorable market conditions and a slower market growth than expected, we have updated our financial forecasts downwards in this update. As a result of the updated forecasts, a contraction in multiples for companies within the cannabis sector and an increase in outstanding shares due to exercise of TO2 warrants and a directed issue, we have updated our valuation range in all scenarios.

6

Value drives

2

Historical profitability

8

Management & Board of Directors

8

Risk profile

All analyses of companies from 2020 onwards are rated based on a new rating system - Value Driver, Historical Profitability and Management & Board ranges from 1 to 10, where 10 is the highest rating. The risk profile ranges from 1 to 10, where 10 is to be considered the highest risk. Stock analyses of companies published before 2020 have been rated based on a different model.

New Products Paves the way for Further Patient Growth

With a new THC/CBD medical cannabis oil approved, which is ready for sales under the Danish pilot program, STENOCARE A/S (“STENOCARE” or the “Company”) has regained the position as the only provider of all three essential oil products under the program; a THC oil, CBD oil, and the new THC/CBD oil. The last time STENOCARE had all three products approved in Denmark back in 2018/2019, the Company reported net sales of DKK 4.3m in Q1-19 with a positive net result. STENOCARE are now back in the same situation in Denmark, and with products approved in five additional markets. With estimated net sales of DKK 66.6m by 2026, and with an applied P/S multiple of 4.5x, a potential present value per share of DKK 8.8 (8.8) is derived in a Base scenario.

- Net Sales Amounted to DKK 1.2m in Q1-24

STENOCARE reported net sales of DKK 1.2m (0.8) in Q1-24, corresponding to a growth of 43% compared to Q1-23. The gross sales, excluding product returns, amounted to DKK 1.4m. With the figures for Q1-24 presented, STENOCARE still has a way to go to reach our estimate of net sales of DKK 16.5m in 2024. However, STENOCARE’s sales fluctuate between quarters as the Company delivers products in large bulks and we expect stronger sales in the coming quarters as sales of the two newly approved products on the Danish and Australian market will be included.

- Operates With a Lean Organization

The operating expenses decreased by 7% in Q1-24 to DKK -4.5m, compared to DKK -4.8m in Q1-23, while the cost base compared to Q4-23 decreased by 12% from DKK -5.1m. Thus, STENOCARE continues to operate with a good cost control towards the estimated break even by the end of 2024.

- German Legalization Enables more Prescriptions

During Q1-24, Germany legalized cannabis for recreational use. Moreover, the country also declassified cannabis as narcotics, something that is expected to simplify the process for more doctors to prescribe medical cannabis and ease the way for patients to obtain a prescription. This is expected to further support the growth of the German medical cannabis market, which is already the largest in Europe with approximately 230,000 patients. STENOCARE entered the German market in Q4-23, and we expect strong sales growth in 2024.

- We make Small Adjustments in our Valuation Range

With reported net sales of DKK 1.2m in Q1-24, we still see possibilities for STENOCARE to reach our revenue estimate of DKK 16.5m in 2024 through sales of the two newly approved products on the Danish and Australian market, as well as sales growth on the German market. Hence, we are keeping our financial forecasts for STENOCARE, as well as a largely unchanged valuation range, with small adjustments in our Bear and Bull scenario.

6

Value drives

2

Historical profitability

8

Management & Board of Directors

7

Risk profile

All analyses of companies from 2020 onwards are rated based on a new rating system - Value Driver, Historical Profitability and Management & Board ranges from 1 to 10, where 10 is the highest rating. The risk profile ranges from 1 to 10, where 10 is to be considered the highest risk. Stock analyses of companies published before 2020 have been rated based on a different model.

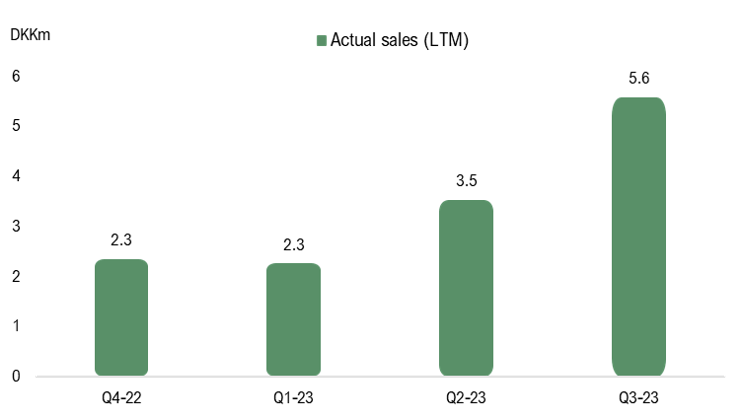

Strong Patient Growth in Denmark

The number of patients continued to grow strongly during Q3-23 for STENOCARE A/S (“STENOCARE” or “the Company”) which resulted in actual sales of DKK 2.3m. The reported net sales amounted to DKK 0.2m but included a large product return from Norway of DKK 2.1m, which we consider as a one-of occasion. Adjusted for the product return, EBITDA amounted to DKK -1.7m, the best in a quarter since Q1-19 and we estimate STENOCARE to reach break-even by the end of 2024. With estimated net sales of DKK 66.6m by 2026, and with an applied P/S multiple of 5x, a potential present value per share of DKK 9.4 (10.2) is derived in a Base scenario.

- Actual Sales Amounted to DKK 2.3m in Q3-23

The reported net sales of DKK 0.2m was affected by a return of products from Norway amounting to DKK 2.1m, which was delivered in Q4-22. Excluding the product return, sales in Q3-23 amounted to DKK 2.3m (0.3), corresponding to a growth of 686% Y-Y, albeit from low levels. The large product return is not desirable, but we expect returns of this size to be a one-off occasion. Excluding the large return from Norway, STENOCARE continues to grow through strong patient growth in Denmark.

- Continues to Operate With a Stable Cost Base

Operating costs amounted to DKK 4.9m in Q3-23, compared to DKK 5.2m in the preceding quarter, why we believe STENOCARE continues to develop with a stable cost base. The EBITDA amounted to DKK -1.7m, adjusted for the returned products, which is the best result since Q1-19 and a step towards the estimated break-even by the end of 2024.

- TO 1 is Important for the Liquidity

STENOCARE’s cash positions amounted to DKK 5m at the end of Q3-23 and based on an estimated burn rate of DKK -0.7m per month, STENOCARE would be financed until early Q2-24, everything else equal. However, the cash position could be strengthened by DKK 3.7-7.8m in gross proceeds through exercise of warrants of series TO 1 in December, with an exercise price between DKK 3.21-6.70. It should also be noted that the Company has convertible bonds maturing on January 1st, 2024, of DKK 7m. However, these can be refinanced or extended, which would delay the maturity, or converted to equity at a share price between DKK 10.89 to 12.13.

- Updated Valuation Range

With figures for Q3-23 presented and an updated guidance from STENOCARE, we have updated our financial forecasts. We have lowered our expectations in international markets as the ramp-up in sales has been slower than estimated. However, we still see continued strong growth in Denmark, break-even at the end of 2024 and a big potential in the Company’s international markets. In this update, we have also switched target year for our valuation to 2026, as STENOCARE is expected to have reached a larger part of the Company’s potential, which, in combination with the updated forecasts results in an updated valuation range in all scenarios.

6

Value drives

2

Historical profitability

8

Management & Board of Directors

7

Risk profile

All analyses of companies from 2020 onwards are rated based on a new rating system - Value Driver, Historical Profitability and Management & Board ranges from 1 to 10, where 10 is the highest rating. The risk profile ranges from 1 to 10, where 10 is to be considered the highest risk. Stock analyses of companies published before 2020 have been rated based on a different model.

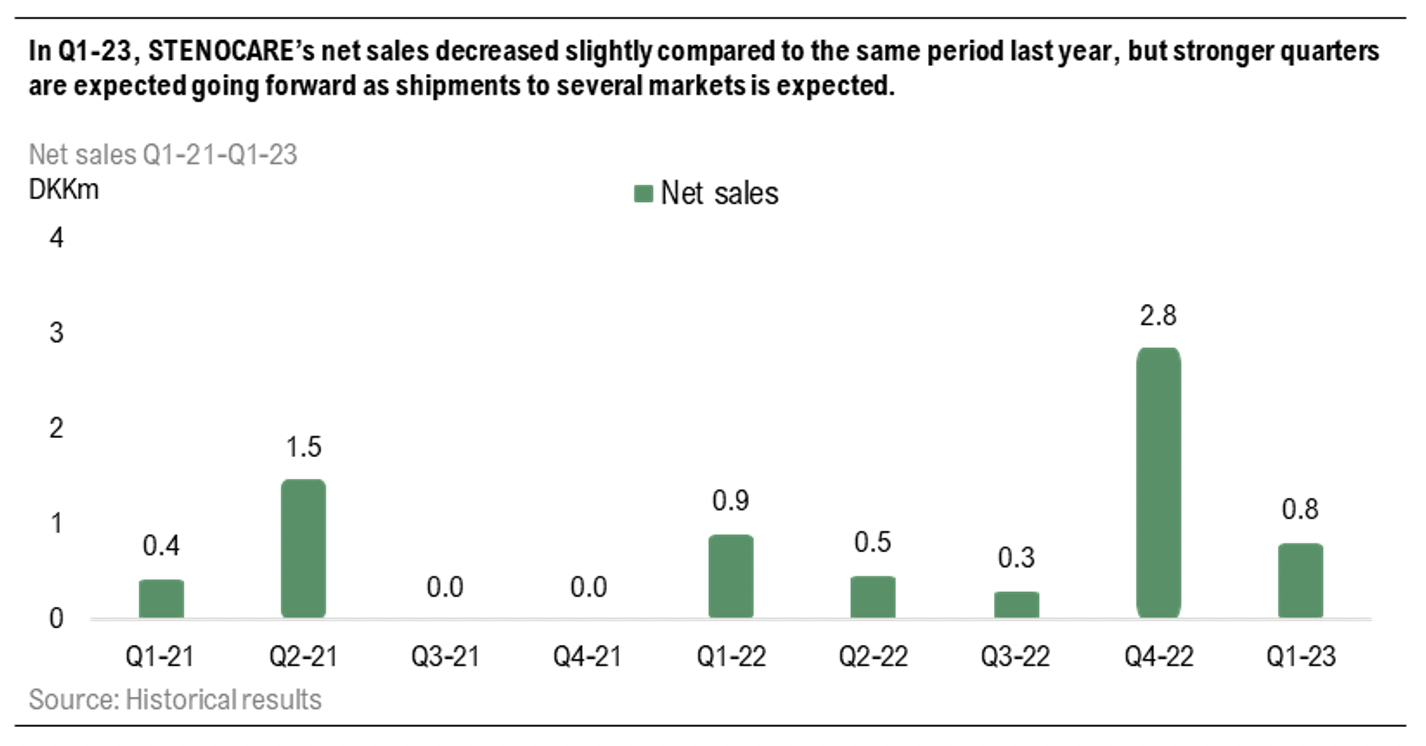

Long-term Sales Drivers are Intact

In Q2-23, STENOCARE delivered a sales growth of 279% Y-Y, amounting to DKK 1.7m with a stable cost development. However, sales growth was under our expectations due to a delay from agencies regarding approval of new products as well as slower sales than expected in international markets. The delay is expected to affect sales growth for the rest of 2023 as STENOCARE’s balanced oil is expected to obtain approval in the end of 2023. This, in combination with other sales drivers such as entering the German market in Q2-23 and a potential launch of the Company’s premium products, is expected to accelerate sales growth from 2024. With estimated net sales of DKK 59.2m by 2025, and with an applied P/S multiple of 5x, a potential present value per share of DKK 10.2 (13.9) is derived in a Base scenario.

- Slower Sales Growth due to Delays from Agencies

STENOCARE’s net sales amounted to DKK 1.7m (0.5) in Q2-23, corresponding to a growth of 279% Y-Y. The development in sales is below our expectations and is, among other things, attributable to a delay from medicinal agencies regarding approving the Company’s products, for instance a balanced oil on the Danish market, which needs approval again as STENOCARE has a new supplier compared to when it was commercially active in 2018/2019. This product has historically represented +50% of the sales volume, why we expect sales growth to accelerate once the new balanced oil is approved, expected in the end of 2023.

- Growth in Prescriptions in Denmark

Despite the balanced oil being delayed, data from the Danish Medicines Agency shows that there has been a growth in the number of patients using medical cannabis since the Company obtained approval for their THC oil (early 2022) and CBD oil (early 2023) respectively. No other oil product has been approved in this period, why we assume that the patient growth is primarily attributable to STENOCARE’s products entering the market, something that is expected to accelerate further when the balanced oil obtains approval.

- Updated Valuation Range

As the figures for the first half year of 2023 is now presented, STENOCARE’s net sales have developed below our expectations. This, in combination with a delay in approval for the balanced oil, which will affect the Company for the rest of 2023, has resulted in an update of our financial forecasts and valuation range in all scenarios. However, we see several growth drivers that are expected to materialize during 2024, including a ramp up in sales in the newly entered German market and a potential launch of the Company’s own premium products, why we still estimate strong revenue growth going forward. In connection with this, we have switched target year for our valuation, why a P/S multiple is applied on 2025 years estimated sales, as STENOCARE is expected to have reached a larger part of the Company’s potential. However, we still see, given today’s share price, that an investment in STENOCARE invites to an attractive risk reward.

6

Value drives

2

Historical profitability

8

Management & Board of Directors

7

Risk profile

All analyses of companies from 2020 onwards are rated based on a new rating system - Value Driver, Historical Profitability and Management & Board ranges from 1 to 10, where 10 is the highest rating. The risk profile ranges from 1 to 10, where 10 is to be considered the highest risk. Stock analyses of companies published before 2020 have been rated based on a different model.

Entering the Largest Market in Europe

With the Q1-report presented, it is clear that STENOCARE A/S (“STENOCARE” or the “Company”), has laid the groundwork for future scale-up, for instance through entering a new market, launching an IT-platform for online clinics as well as selecting a partner to produce the Company’s premium products. Sales is expected to fluctuate from quarter to quarter due to products being shipped in large quantities, why we expect stronger revenues in the coming quarters than the DKK 0.8m presented in Q1-23. With estimated net sales of DKK 60.4m by 2024, and with an applied P/S multiple of 5.5x, a potential present value per share of DKK 13.9 (21.4) is derived in a Base scenario.

- Entering the German Market

STENOCARE has obtained approval for a new product in Germany, which is by far the largest market for medical cannabis in Europe, with estimated sales of EUR 1bn by 2027, compared to EUR 2.2bn for Europe in total. Given the German markets size, this also entails more competition, where STENOCARE’s competitive advantage is expected to be that the Company’s product will be reimbursed by insurance companies, which is not the case for all products.

- Decrease in Sales – Improvement Expected Ahead

STENOCARE’s net sales during Q1-23 amounted to DKK 0.8m (0.9), a decrease of 10% compared to Q1-22. Given that sales is expected to fluctuate from quarter to quarter due to bulk deliveries and that STENOCARE delivered products to five markets in Q4-22, we do not attach great importance to this and estimates stronger sales in the coming quarters.

- Capital Injection Intensifies the Growth Focus

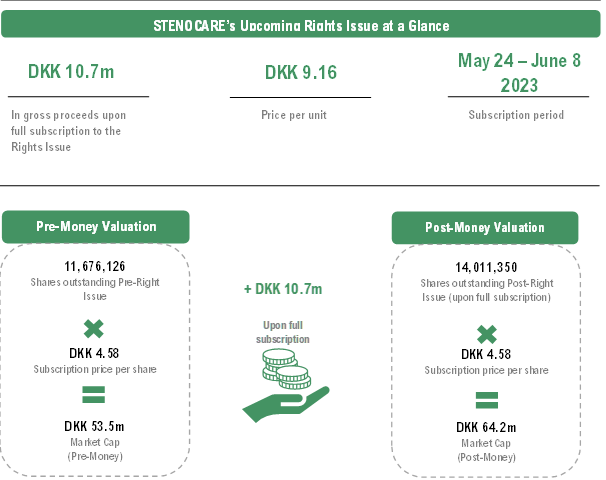

During June 2023, STENOCARE raised DKK 10.7m in gross proceeds through a unit rights issue which was oversubscribed. The funds will be used to further scale the core business and complete the indoor cultivation facility, something that we expected the Company to complete without further capital injections, hence, the investments needed for this appears to be higher than we estimated. However, we believe that the capital injection puts STENOCARE in a greater position to scale up sales by obtaining approvals in new markets and increase commercial efforts in current markets as well as strengthening the balance sheet, why we believe the Company is in a good position to deliver strong revenue growth going forward.

- Updated Valuation Range

With the Q1-report presented, we are repeating our forecasts in a Base and a Bull scenario, however slightly more conservative estimates are made in a Bear scenario. Moreover, we have seen a multiple contraction among peers since our latest update, which results in a lower valuation multiple for STENOCARE in all scenarios. This, together with the capital injection from the unit rights issue and directed issue for debt conversion, which entailed an increase in outstanding shares, results in an updated valuation range in all scenarios.

6

Value drives

2

Historical profitability

8

Management & Board of Directors

6

Risk profile

All analyses of companies from 2020 onwards are rated based on a new rating system - Value Driver, Historical Profitability and Management & Board ranges from 1 to 10, where 10 is the highest rating. The risk profile ranges from 1 to 10, where 10 is to be considered the highest risk. Stock analyses of companies published before 2020 have been rated based on a different model.

Capitalizing on the Growing Cannabis Market

After entering three new markets in 2022, STENOCARE delivered products to a total of five countries during Q4-22, leading to net sales amounting to DKK 2.8m. This is the best revenues presented since Q1-19, before the resolved issues with STENOCARE’s former supplier, CannTrust, started. The Company has 11 products approved in these five countries and are expected to continue the geographical expansion. Operating on a market with strong expected growth due to further deregulations throughout Europe, Analyst Group believes that the Company is in a great position to deliver strong revenue growth going forward. With estimated net sales of DKK 60.4m by 2024, and with an applied P/S multiple of 7x, a potential present value per share of DKK 21.4 (21.4) is derived in a Base scenario.

- Further Legalization can Expand the Market

The European cannabis market has an exiting year ahead, with a potential legalization of adult use1 in Germany as a highlight. Such a legalization is expected to act as a catalyst for more countries to ease regulations and create a broader acceptance towards medical cannabis, which would create further market growth. Legal cannabis sales in Europe are expected to grow with a CAGR of 67% until 2025, amounting to EUR 3.2bn, driven by legalization of both medical and adult use. Accordingly, STENOCARE is expected, in the long run, to capitalize on the continued deregulation on the European market.

- Adapting to the Current Market and Regulations

STENOCARE is now the sole supplier of full spectrum medical cannabis oil products in Denmark, Norway and Sweden, which Analyst Group sees as a result of the Company’s competence in relations to regulations and delivering quality products, by using indoor cultivation facilities rather than green houses. Going forward, we see this as a crucial factor to operate within the highly regulated European market. Furthermore, STENOCARE has designed its logistical procedures according to the Company’s distribution partners, which is delivering in larger quantities. This is expected to lead to fluctuation in sales, while being a competitive advantage for STENOCARE.

- Launch of Premium Products Ahead

STENOCARE’s premium products, which are expected to be launched during 2024 are using a targeting lymphatic absorption technology that enable an enhanced uptake of the drug in the blood, regardless of food intake as well as a faster effect. Given that these products are approved, STENOCARE is expected to have a unique product on the market compared to current alternatives, leading to accelerated sales.

- Our Valuation Range Stands

The year-end report was in-line with our expectations, why we repeat our revenues forecast and valuation range. However, slight adjustments has been made regarding the cost development in the forecasts.

6

Value drives

2

Historical profitability

8

Management & Board of Directors

6

Risk profile

All analyses of companies from 2020 onwards are rated based on a new rating system - Value Driver, Historical Profitability and Management & Board ranges from 1 to 10, where 10 is the highest rating. The risk profile ranges from 1 to 10, where 10 is to be considered the highest risk. Stock analyses of companies published before 2020 have been rated based on a different model.

The Pharmaceutical Approach

After several years of work ensuring a good supply chain and getting products approved on five different markets, STENOCARE is now ready to launch 11 full spectrum medical cannabis oil products in five regulated countries. Operating in an industry with strong expected growth and considering the future launch of STENOCARE’s own premium products, which are expected to have several benefits compared to competing products, Analyst Group estimates exponential revenue growth going forward. With estimated net sales of DKK 60.4m by 2024, and with an applied P/S multiple of 7x, a potential present value per share of DKK 21.4 is derived in a Base scenario.

- A Cannabis Company With a Pharma Attitude

Since the Danish Pilot Program, enabling doctors to prescribe medical cannabis, started on January 1st, 2018, STENOCARE is the only player on the market getting medical cannabis oil products approved by Danish authorities. This is, according to Analyst Group, a result of the Company’s ability to manage regulations and deliver quality products, for example through using indoor cultivation facilities rather than green houses. Going forward, we see this as a crucial factor to operate within the highly regulated European market.

- A new Market With big Potential

The medical cannabis market in Europe is still in its early days, although more countries are legalizing. Legal cannabis sales in Europe are expected to grow with a CAGR of 67% until 2025, amounting to EUR 3.2bn, driven by continued legalization of both medical and adult use.2 STENOCARE is expected to capitalize on these market trends through increased patient prescriptions, contributing to increased sales, driven by the health care industry having a greater acceptance of the benefits compared to competing treatments.

- Launch of Premium Products

STENOCARE is developing their own premium products, which are expected to solve several well-known product deficiencies that other industry players struggle with. The premium products is using a targeting lymphatic absorption technology, that enable an enhanced uptake of the drug in the blood, regardless of food intake as well as a faster effect. Given that these products are approved, STENOCARE is expected to have a unique product on the market compared to current alternatives.

- Highly Regulated Market

Today, STENOCARE has 11 products approved in five regulated countries. A critical factor going forward is to obtain the necessary approvals to import and sell on new markets, which is a challenge. However, STENOCARE has a strong track record of entering new markets, which we see as a clear Proof of Concept.

6

Value drives

2

Historical profitability

8

Management & Board of Directors

6

Risk profile

All analyses of companies from 2020 onwards are rated based on a new rating system - Value Driver, Historical Profitability and Management & Board ranges from 1 to 10, where 10 is the highest rating. The risk profile ranges from 1 to 10, where 10 is to be considered the highest risk. Stock analyses of companies published before 2020 have been rated based on a different model.

Analyst Comments

Comment on the Outcome of STENOCARE’s Conditional Rights Issue

2025-01-22

On January 22nd, STENOCARE announced the outcome of the conditional rights issue, which was subscribed to approximately 37.7%. Moreover, guaranteed commitments from Exelity AB amounting to 7.3% will be activated to achieve a subscription rate of 45%, which will provide STENOCARE with DKK 9.1m in gross proceeds in order to execute on the STENOCARE 3.0 strategy.

Analyst Group’s View of the Outcome

The rights issue will provide STENOCARE with DKK 9.1m in gross proceeds and with estimated transaction-related costs amounting to DKK 0.9m and guarantor compensation of DKK 0.3m, the estimated net proceeds amount to DKK 7.9m. With the new STENOCARE 3.0 strategy the company is transforming into a trading company, focusing on distribution of prescription-based medical cannabis and hence exiting production activities, the proceeds are expected to be used for commercial activities linked to the company’s existing product portfolio, which consists of 13 approved products in six countries. STENOCARE has already established key assets (regulatory, supply chain, commercial, partnerships), that will be the foundation for the new strategy. The medical cannabis market has proven challenging to penetrate, partly due to high competition and partly due to widespread skepticism toward cannabis among prescribing doctors. STENOCARE is therefore expected to place greater focus on educating doctors about the benefits of medical cannabis treatment, thereby driving growth.

We see the company’s premium product Astrum oil as an important growth driver in the coming year, as it distinguishes STENOCARE from competitors as a first mover in the next generation of medical cannabis, providing improved, uniform and faster uptake in the blood. During 2024, STENOCARE announced that the Astrum oil has been approved for sales in three countries, Australia, Germany and Norway, which we see as the most important growth driver, particularly as Australia and Germany are two of the largest medical cannabis markets globally. Furthermore, STENOCARE is expected to receive approvals in additional markets going forward, since the company has a strong track record of market approvals.

In addition to the commercial activities, part of the net proceeds is expected to be used for servicing the convertible loan of DKK 2.8m with interests and installments. Going forward, as STENOCARE has decided to exit its production activities, substantial cost savings are expected going forward, equivalent to DKK 4m annually in 2025 for personnel and other expenses, as well as long-term lease and equipment lease amounting to DKK 14m over the next six years. This is expected to reduce the company’s burn rate going forward and contribute to a shorter path toward achieving positive cash flow.

Considering challenging market conditions, where many smaller companies face difficulties in raising capital under favorable terms, Analyst Group considers the outcome of the rights issue reasonable.

Subscription Rate and Dilution

The rights issue was subscribed to approximately 37.7%, including the pre-subscription commitments and compensation free guarantees of 7.4%. As a result, guarantor commitments of 7.3% will be activated to achieve a subscription rate of 45%, corresponding to 18,191,248 new shares and STENOCARE will receive DKK 9.1m in gross proceeds. Transaction related costs are estimated at DKK 0.9m plus guarantor compensation of DKK 0.3m, which results in estimated net proceeds of DKK 7.9m.

As mentioned, the total number of shares will increase by 18,191,248 new shares, from 20,212,497 shares to 38,403,745 shares, why the dilution effect for shareholders who did not participate in the rights issue amounts to approximately 47.4%.

In summary, we view the outcome of the rights issue as reasonable, given the current market climate. We expect STENOCARE to utilize the net proceeds, in addition to repaying the loan, to scale up sales, including education on the benefits of the new innovative Astrum oil. After several sales-challenging years for STENOCARE, partly due to a more sluggish market than expected, it is critical for the company to prove the company’s ability to increase sales in different markets. We see the new wholehearted focus on becoming a distributor, and the benefits of Astrum oil, as important factors for achieving this success.

Comment on STENOCARE’s Announcement of a Conditional Rights Issue of up to DKK 20.2m

2024-12-20

On December 18th, STENOCARE announced that the company has resolved a rights issue of up to DKK 20.2m at a subscription price of DKK 0.5. The capital increase is conditional upon a minimum of a total subscription rate of approximately 45 percent, providing the Company with approximately DKK 9.1m before deduction of transaction related costs. STENOCARE has received legally binding written pre-subscription commitments and compensation free guarantees from management and existing shareholders of DKK 1.5m, corresponding to approximately 7.4% of the total Rights Issue.

The rights issue will offer existing shareholders two subscription rights for each share held, with each right enabling the purchase of one new share at a price of DKK 0.5. The subscription period runs from January 7 to January 20, 2025, and the offering is contingent upon a minimum subscription of 18,191,248 shares, equivalent to approximately 45% of the issue, which would provide STENOCARE with approximately DKK 9.1m in gross proceeds before deduction of transaction-related costs estimated at DKK 0.9m. If fully subscribed, the company will raise DKK 20.2m before transaction costs, which are estimated at DKK 1.7m, leaving net proceeds of DKK 18.5m.

The proceeds will be used to fund commercial activities, including the launch of STENOCARE’s innovative ASTRUM 10-10 medical cannabis product in key markets like Australia, Germany, and Norway. The company’s new strategy, STENOCARE 3.0, focuses on becoming a trading entity, ceasing its in-house cultivation to reduce costs significantly. This pivot is expected to save approximately DKK 14m in lease obligations and DKK 4m annually in operating costs. Additionally, the proceeds will be used to service the convertible loan of DKK 2.8m with interests and installments.

Analyst Group’s view of the Rights Issue

Analyst Group has previously highlighted STENOCARE’s strained financial position in earlier updates, where a share issue was regarded as the most likely scenario. The company has also communicated that it has been exploring various financing options, making the announced rights issue no significant surprise. However, the weak stock performance during the last months, which is likely affected by the uncertainty regarding the financial position, and the current financial market environment for capital raises is resulting in a substantial stock dilution of 67% given full subscription for shareholders who chooses not to subscribe, which is not a positive aspect for the shareholders in the short term. Going forward, the proceeds are necessary for STENOCARE to execute on planned commercial activities with the launch of the Astrum oil in several markets seen as the most important growth driver. Given that the net proceeds are expected to be used for commercial activities, except the repayment of debt of DKK 2.8m, the capital raise is expected to strengthen the revenue outlook for the company.

As the STENOCARE 3.0 strategy focuses on becoming a trading company and exit from cultivation activities, we expect a significantly decreased cost base going forward, which is why more focus and capital are expected to be directed toward increasing sales of the products that STENOCARE currently has on the market, comprising 13 products across six countries. The medical cannabis market has proven challenging to penetrate, partly due to high competition and partly due to widespread skepticism toward cannabis among prescribing doctors. STENOCARE is therefore expected to place greater focus on educating doctors about the benefits of medical cannabis treatment, thereby driving growth.

Furthermore, STENOCARE addresses the challenges of high competition and the stigma among doctors regarding medical cannabis with its Astrum oil product. This innovative and patented product is expected to improve the uptake in the blood and deliver a uniform uptake in the blood across individuals and regardless of food consumption, unlike other medical cannabis products. Historically, doctors have encountered challenges when prescribing medical cannabis to patients due to the body’s metabolism, which significantly reduces the uptake of cannabinoids. Astrum oil thereby facilitates decision-making for doctors and differentiates STENOCARE from its competitors, making the product a key growth driver for the company.

In summary, the announced rights issue was anticipated; however, given the weak share price and challenging market conditions for capital raising, it results in a dilution effect of 67% for shareholders who choose not to participate, assuming full subscription. With a subscription price of DKK 0.5 per share, this corresponds to a pre-money valuation of DKK 10.1m. Considering the opportunities associated with an increased commercialization focus on Astrum oil, which is expected to drive expansion into additional markets, Analyst Group views the announced rights issue as an attractive investment opportunity.

Comment on STENOCARE’s Approval for a new Medical Cannabis CBD100 oil

2024-12-17

On December 17th, STENOCARE announced that the company has received approval for a new product in Denmark, CBD100, which has a high concentration of CBD active ingredients (100 mg/ml). This makes STENOCARE the only supplier to offer a CBD100 oil product in Denmark.

With the CBD100 oil product added to the portfolio, STENOCARE’s portfolio consists of four products approved for sales in Denmark, including a lighter CBD-oil, a THC-oil and a balanced oil, which solidifies the company’s position as a leading supplier in the country, which recently formally agreed on permanent legalization of medical cannabis.

The new product, CBD100, has a higher concentration of CBD, which targets patients who need higher dosages in its treatment. CBD can be used as a treatment for a range of symptoms, including chronic pain, anxiety, stress, and nausea experienced by cancer patients during treatments, thereby addressing several significant and widespread symptoms affecting numerous patients. The new CBD oil provides doctors in Denmark with an additional option for treating these symptoms, as STENOCARE becomes the sole supplier of medical cannabis oil products with such a high concentration of CBD, which, according to Analyst Group, constitutes a competitive advantage.

STENOCARE has a strong track record of getting products approved in several markets, both highly regulated and markets with lower barriers to entry, which the approval of the CBD100 oil product further solidifies. This is expected to be beneficial in the company’s new strategy, aiming to be a leading trading company for medical cannabis products with broad range of products to reach more patients and hence deliver growth in sales.

In summary, we view positively on the news of the approved CBD100 oil product, as it further solidifies STENOCARE’s position as a leading supplier in Denmark and provides an additional option for doctors and patients in Denmark, as this is the only medical cannabis oil product with this concentration of CBD, which is seen as a competitive advantage.

Comment on that STENOCARE’s Astrum Oil has been Approved for Sales in Norway

2024-12-02

STENOCARE announced on December 2nd that the company’s premium product, the Astrum oil, has been approved for sales on the Norwegian market. The product is expected to have several benefits compared to the medical cannabis oil available today, including a higher, more uniform, and faster uptake in the blood. The product, Astrum 10-10 oil Stenocare, with 10 mg/ml THC and 10 mg/ml CBD, is expected to be available for patients in Norway within the next 30 days.

The Benefits of the Astrum Oil

Today, doctors encounter challenges when prescribing medical cannabis to patients due to the body’s metabolism, which significantly reduces the uptake of cannabinoids to approximately 15%. This results in only a variable and often minimal portion of the cannabinoids being actively delivered to the body with therapeutic effect, meaning an inconsistent uptake of the active ingredients into the blood. Additionally, the absorption by the body varies from person to person and depending on whether the medication is taken before or after food consumption. This variability leads to unpredictable effects and complicates the doctors’ ability to prescribe the correct dosage.

STENOCARE’s new Astrum oil addresses all of these problems as it is based on a new innovative oil technology. In H2-22, STENOCARE released a study in dogs, showing that the Astrum oil improves the uptake in the blood with a factor of 2.6 compared to a reference MCT-oil product in the market. Moreover, the Astrum oil delivers a uniform uptake in the blood across individuals and regardless of food consumption. Lastly, the Astrum oil improves the time from dosing to full effect from 2-4 hours to just 1 hour, an important step to help patients manage their medical problems.

Analyst Group’s View of the Approval

With the launch of the Astrum oil, which has previously been approved in Australia and Germany, we see STENOCARE as a first mover in next generation medical cannabis oil products. STENOCARE are dependent on doctors prescribing the company’s products and considering the advantages of the Astrum Oil, we expect doctors to appreciate the new product. The Astrum oil is expected to be a more predictable medical cannabis product, helping doctors to prescribe the correct dosage.

As we see the Astrum oil as the most important value driver, we view positively on the approval since it further proves the need. Moreover, the launch on the Norwegian market increases the availability of the product for patients and facilitate for doctors. However, the Norwegian market is significantly smaller than the German and Australian markets, both in terms of number of addressable patients due to lower population and since it is a highly regulated market, where it remains difficult to obtain access to medical cannabis, with many patients that are thought to turn to the black market instead.

Furthermore, STENOCARE has historically encountered challenges with the highly regulated Norwegian market. In Q4-22, STENOCARE made the first shipment of full spectrum medical cannabis oil products to the company’s Norwegian partner, Apotek 1, for sales in the Norwegian market. However, the management of the pain centers (hospitals) unexpectedly decided to hold back the budget for treatment with all cannabis-based products, which hampered sales and consequently led to product expiration. As a result, products worth of DKK 2.1m were returned to STENOCARE. However, we expect that STENOCARE has implemented new procedures to secure the largest possible assurance of sales to patients prior to delivery to all new markets in the future. The updated procedures are expected to reduce the risk of similar large volume expirations going forward.

Nevertheless, the approval once again demonstrates STENOCARE’s ability to secure product approvals in highly regulated markets. The company has thus reaffirmed its capacity to obtain approvals across all types of markets, which we regard as a strength for future expansion into additional markets with Astrum oil.

In summary, Analyst Group views positively on STENOCARE’s approval of the Astrum oil in the Norwegian market even though the market is expected to have a significantly smaller financial impact than the approval on the German and Australian, due to the higher regulated market as well as the smaller population, hence the number of addressable patients. Nevertheless, it demonstrates the ability to secure product approvals in highly regulated markets, which we view as advantageous for the continued expansion of Astrum oil and is expected to make the product available for more patients, which we see as the most important growth driver for STENOCARE going forward.

Comment on STENOCARE Shifting Strategy to Focus on Trading and Exit from Production

2024-11-27

STENOCARE announced on November 26th the STENOCARE 3.0 Strategy, which means that the company will focus on trading prescription-based medical cannabis sourced from suppliers and exit the production activities at STENOCARE’s own indoor cultivation facility. The decision is based on prolonged and uncertain approval timelines with the Danish Medicines Agency, which creates difficulties in establishing a reliable timeline for the facility’s approval. This exit will eliminate approximately DKK 18m in cost obligations over the next six years.

When the legalization of medical cannabis began in Europe in 2017, quality and legal requirements were established to mirror pharmaceutical standards, why STENOCARE deemed it crucial to control the entire value chain to ensure the highest possible product quality. However, the indoor cultivation facility has been delayed, and there is still no clear timeline for approval from the Danish Medicines Agency. At the same time, the production facility involves high costs and is capital-intensive, prompting STENOCARE to discontinue production. In-house production has proven to be too capital-intensive for smaller players in the market, leaving only larger companies able to sustain a fully integrated value chain, a trend that is expected to continue over the next year.

STENOCARE’s current financial position is assumed to have influenced the decision, as the cash balance at the end of Q3-24 amounted to DKK 0.1 million, a plan for the company’s future funding is expected to be announced soon. While STENOCARE will not receive any payment for transferring the production facility, the company will be relieved of all related costs, including the significant long-term lease and equipment lease. This represents a financial obligation of approximately DKK 14m over the next six years, which will no longer weigh on the company. Furthermore, STENOCARE will achieve annual savings of approximately DKK 4m in production staff and operating costs during 2025.

STENOCARE has signed a conditional agreement with Hedemann Løvstad Ejendomsselskab ApS (HLE) to end the lease contract for the cultivation facility. As part of this agreement, ownership of production equipment will be transferred to HLE, but the agreement is conditional upon STENOCARE’s success in raising capital.

According to Analyst Group, the discontinuation of production is a positive development for STENOCARE’s financial position, which is currently strained. Despite the company’s historical investments in the facility, substantial cost savings is to be expected in the coming years. Furthermore, we believe that the company’s key growth and value drivers remain intact, primarily via the innovative ASTRUM oil, which is approved for sale in Australia and Germany as of now, furthermore the sale of prescription-based medical cannabis oil products in six countries. Among these, Denmark, Australia, and Germany are considered the most promising markets, despite the current challenges in Denmark stemming from increased competition and a unique situation involving a competing magistral product subsidized at 85% for patients by the Danish Medicines Agency, compared to STENOCARE’s 50%. As a result, STENOCARE is focusing on transitioning into a trading company, where there is greater growth opportunities and improved profitability.

Comment on the Danish Health Minister’s Decision to Propose a Permanent Legalization of Medical Cannabis

2024-11-20

Medical cannabis has been legal in Denmark under a pilot program since 2018 during a trial period that was set to expire in December 2025. However, on November 19th, the Danish Health Minister invited political parties to discuss the permanent legalization of medical cannabis in Denmark, where STENOCARE has three medical cannabis oil products approved for sale. The intention of the government is to proceed with the legalization.

The government in Denmark is proposing to make the pilot program permanent and has invited political parties to discuss the matter. According to a press release from the Minister for Interior and Health, this is based on a new evaluation which shows that the number of redeemed prescriptions has increased significantly and is now at its highest level since 2018. According to The Minister of Interior and Health, Sophie Løhde, many patients has benefitted from the treatment of medical cannabis, for instance cancer patients who may suffer from severe nausea after chemotherapy treatment, or people with multiple sclerosis who may experience severe pain.

The potential permanent legalization will enable continued treatment with medical cannabis for patients and provide clarity regarding the future of the industry in the country.

Analyst Group’s view of the impact on STENOCARE

Analyst Group views this as positive news for STENOCARE, a leading supplier of medical cannabis products to the Danish Pilot Programme since 2018. With potential permanent legalization, a clear future will be established for STENOCARE in the country, further justifying investments in new products. For instance, the company’s innovative new product, Astrum oil, which according to Analyst Group has the potential to revolutionize the industry, has been approved in Australia and Germany, and we now see Denmark as the next potential market for the product.

The Danish market has been STENOCARE’s home market and its most important in terms of sales historically, as the company is expected to have a strong brand among doctors in the country. Hence, we see good potential for STENOCARE to grow in the market, even though a special situation with a competing magistral product, which is supported by an 85% patient subsidy from the Danish Medicines Agency, is expected to hamper sales growth in the short term.

In summary, legalization eliminates a source of uncertainty for STENOCARE, paving the way for continued investments in the country, which is one of the company’s most important markets.

Comment on STENOCARE’s Q3-Report 2024

2024-11-06

STENOCARE published on November 5th the company’s Q3-report for 2024. The following are some key points that we have chosen to highlight in connection with the report:

- Continued challenging market affected sales

- A decreased cost base to adapt to the slower sales

- Additional funding needed to leverage market potential

Challenging Market Conditions Continued During Q3-24

The gross sales amounted to DKK 1.1m (2.4) in Q3-24, corresponding to a decrease of 53 %. Net sales were affected by returns of expired products amounting to DKK 2m, leading to net sales amounting to DKK -0.9m (0.2). The expired return products is assumed to be primarily attributable to the Danish market, where the company are experiencing increased competition and a special situation with a competing magistral product being supported with 85% patient subsidy from the Danish Medicines Agency, compared to STENOCARE’s 50%. This has led to slower sales than expected as well as expired products being returned to the company. STENOCARE are exploring various avenues to address this situation, including a dialogue with the medicines agency but the situation is unchanged and expected to affect the company throughout the rest of 2024.

Additionally, STENOCARE had products returned from UK and Norway, delivered in Q3-23, due to expiry, indicating that demand has been lower than expected in these countries as well. This is anticipated to be due to that the integration of medical cannabis into clinical practice has not progressed as rapidly as was anticipated a few years ago as well as increased competition.

STENOCARE has long addressed the increasing competition by initiating the development of a new, innovative product, now named Astrum Oil, which has been approved for sale in Australia and Germany. The product is expected to have several benefits compared to the medical cannabis oil available today, including a higher, more uniform, and faster uptake in the blood. With this launch, we see STENOCARE as a first mover in next generation medical cannabis oil products, why we see that the company can gain an advantage against competitors. The product is expected to be available for patients from Q4-24.

In summary, there are several short-term sales challenges, however, given the advantages of the company’s innovative Astrum Oil, STENOCARE is still considered to have strong potential for substantial revenue growth in the longer term.

Additional Cost Savings in a Tough Market

The operational expenses amounted to DKK 3m (4), corresponding in a decrease of 26%. Cost of goods sold is included in the external expenses and due to the lower gross sales in Q3-24 compared to last year, the cost of goods sold has decreased, explaining part of the decrease. Additionally, we believe that STENOCARE has continued to optimize the company’s cost structure to reduce the burn rate, given the lack of sales acceleration so far, which we view positively on.

Plan to Adress the Capital Requirements for Future Growth Expected

STENOCARE’s cash position amounted to DKK 0.1m at the end of Q3-24 and the company stated in the Q3 report that the plan for future funding of the company will be announced soon. During Q3-24 the cash flow from operating activities amounted to DKK -1.9m and was positively affected by DKK 2.2m through change in working capital. The main explanation for the positive effect is the increase in the item “Other payables”, where we could see a similar effect in Q3-23, when STENOCARE also had product returns. The effect was later reversed in Q4-23, why we expect this to have a similar negative effect on the cash flow in the upcoming fourth quarter.

As mentioned in our previous updates regarding STENOCARE, the company will need to secure additional funding to enable future growth initiatives such as the launch of Astrum oil. We consider the most likely option to be a capital raise, however, given the recent weak stock performance, such a capital raise could incur under unfavourable conditions for existing shareholders.

To summarize, STENOCARE continues to experience challenges regarding market conditions through increased competition, higher subsidy on a competing product in Denmark and an overall slower market growth than expected, which has affected sales. We expect these challenges to remain in the short term but consider the company’s Astrum oil as a potential strong sales driver in the longer term given the advantages of the product for industry. STENOCARE continues to optimize the cost base to adapt to the current market but will need additional funding going forward, where we expect a plan regarding the future capital requirements to be announced soon.

We will return with an updated equity research report of STENOCARE.

Comment on STENOCARE’s Updated Guidance for 2024

2024-10-14

STENOCARE announced on October 14th that the company has updated the sales guidance for 2024, from gross sales of DKK 6-8m, which are now expected to amount to DKK 4.5m. STENOCARE is also exploring various financing opportunities to meet both short-term and long-term capital needs.

The primary reason for the updated guidance is the unfavorable market conditions that were mentioned in connection with the Q2 report in August, which persisted throughout Q3 and led to lower sales than anticipated. The unfavorable market conditions mentioned include a decrease in product prices and increased competition due to higher product price subsidies on magistral products in Denmark, which has not been resolved during Q3-24. Additionally, the company has experienced returns on expired products amounting to approximately DKK 2m, which were initially delivered to meet expected demand and will affect the Q3 results.

Analyst Group’s view

As mentioned in connection with the Q2 report, STENOCARE entered 2024 with several potential growth drivers, including the balanced oil approved in Denmark, a new product in Australia, and entry into the German market. However, these have not delivered the expected growth, even though the company has successfully made the planned strategic progress in these countries. This is believed to be due to the integration of medical cannabis into clinical practice not progressing as rapidly as anticipated a few years ago. Moreover, market conditions in Denmark have impacted sales in the country and resulted in product returns. Gross sales are expected to amount to DKK 1.1m, and with product returns of DKK 2m, this implies negative net sales of approximately DKK -1m in Q3-24. STENOCARE has revised the company’s logistical supply principles together with local pharma distributors to minimize the future risk of product returns in the Danish market.

In our latest equity research report, we had estimated net sales of DKK 6m for 2024. Considering the updated guidance as well as the product returns of DKK 2m, we expect to lower this estimate in connection with our next update following the Q3 report. Nevertheless, STENOCARE is expected to deliver the new premium Astrum oil to both Germany and Australia in Q4, which is expected to offer several benefits compared to the medical cannabis oil available today, including higher, more consistent, and faster absorption into the bloodstream. With this launch, we see STENOCARE as a first mover in next-generation medical cannabis oil products, which we believe will give the company a competitive advantage. The Astrum oil is expected to become an important sales driver going into 2025.

Lastly, STENOCARE is considering a range of financing options to address the company’s capital needs in both the short and long term, with more details expected to be announced soon. In our analysis following the Q2 report, we mentioned that we believe STENOCARE will need to secure additional funding, most likely through a capital raise, to enable future growth initiatives such as the launch of Astrum oil. However, given the recent weak stock performance, such a capital raise could incur under unfavorable conditions for existing shareholders.

Comment on STENOCARE’s Q2-report Report 2024

2024-08-22

STENOCARE published on August 21st the company’s Q2-report for 2024. The following are some key points that we have chosen to highlight in connection with the report:

- Financial development during the period

- Launch of premium products ahead of plan

- Financial position and burn rate

Sales Lower than Expected due to Unfavourable Market Dynamics Concerning Pricing and Reimbursement Principles

STENOCARE’s net sales amounted to DKK 0.7m (1.7), corresponding to a decrease of 57% compared to Q2-23, which was below Analyst Group’s expectations. The lower than anticipated sales are, among other things, a result of a decrease in product prices and increased competition due to higher product price subsidy in Denmark, as well as slower sales in international markets. STENOCARE had several growth drivers going into 2024, including the balanced oil approved in Denmark, a new product in Australia and entering the German market, which has not delivered growth as expected, even though the company has successfully made the planned strategic progress in these countries. This is anticipated to be due to the integration of medical cannabis into clinical practice has not progressed as rapidly as was anticipated a few years ago.

Based on the financial performance and the outlook for 2024 STENOCARE announced on August 20th that the company updates the guidance for 2024, from gross sales of DKK 12-18m to DKK 6-8m and that the expected break even at the end of 2024 is no longer realistic. The revised guidance is primarily based on the earlier mentioned increasing competition and the dynamic pricing model in Denmark, which has entailed a decline in prices and hence affected STENOCARE’s net sales, even though the company expects to deliver +20% more products units in Denmark during 2024. Even though sales are expected to improve in H2-24 compared to H1-24 we are likely to update our financial forecasts for STENOCARE based on the financial performance in Q2-24 as well as the updated guidance.

The Cost Base Continues to Decrease

The operational expenses, excluding depreciation, amounted to DKK -3.5m (-4,3), corresponding to a decrease of 19%. Thus, we believe that STENOCARE is continuing to optimize its cost structure to reduce the company’s burn rate, given the lack of sales acceleration so far, which we view positively.

Launch of Premium Products Ahead of Plan

During Q2-24, STENOCARE announced that the company’s premium product, the Astrum oil, is ready for launch on the Australian market. The product is expected to have several benefits compared to the medical cannabis oil available today, including a higher, more uniform, and faster uptake in the blood. With this launch, we see STENOCARE as a first mover in next generation medical cannabis oil products, why we see that the company can gain an advantage against potential competitors. After the end of the period, on July 31st, STENOCARE announced that the Astrum oil has been approved in Europe’s largest medical cannabis market, Germany.

Moreover, STENOCARE also announced that the company is looking into an expansion to Canada. The Canadian market is a vast market with a lot of competition but with STENOCARE’s premium product Astrum, Analyst Group believes that STENOCARE can position the company’s products within a distinct niche, even in the most competitive markets such as the Canadian, because of the unique benefits with the products patented oil technology. This enables STENOCARE to become one of the few European companies capable of capitalizing on one of the largest medical cannabis markets globally.

Stable Patient Development in Denmark

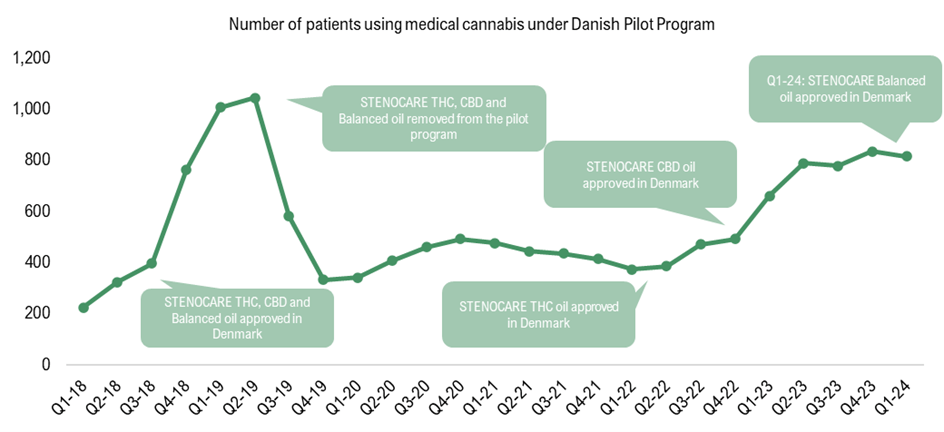

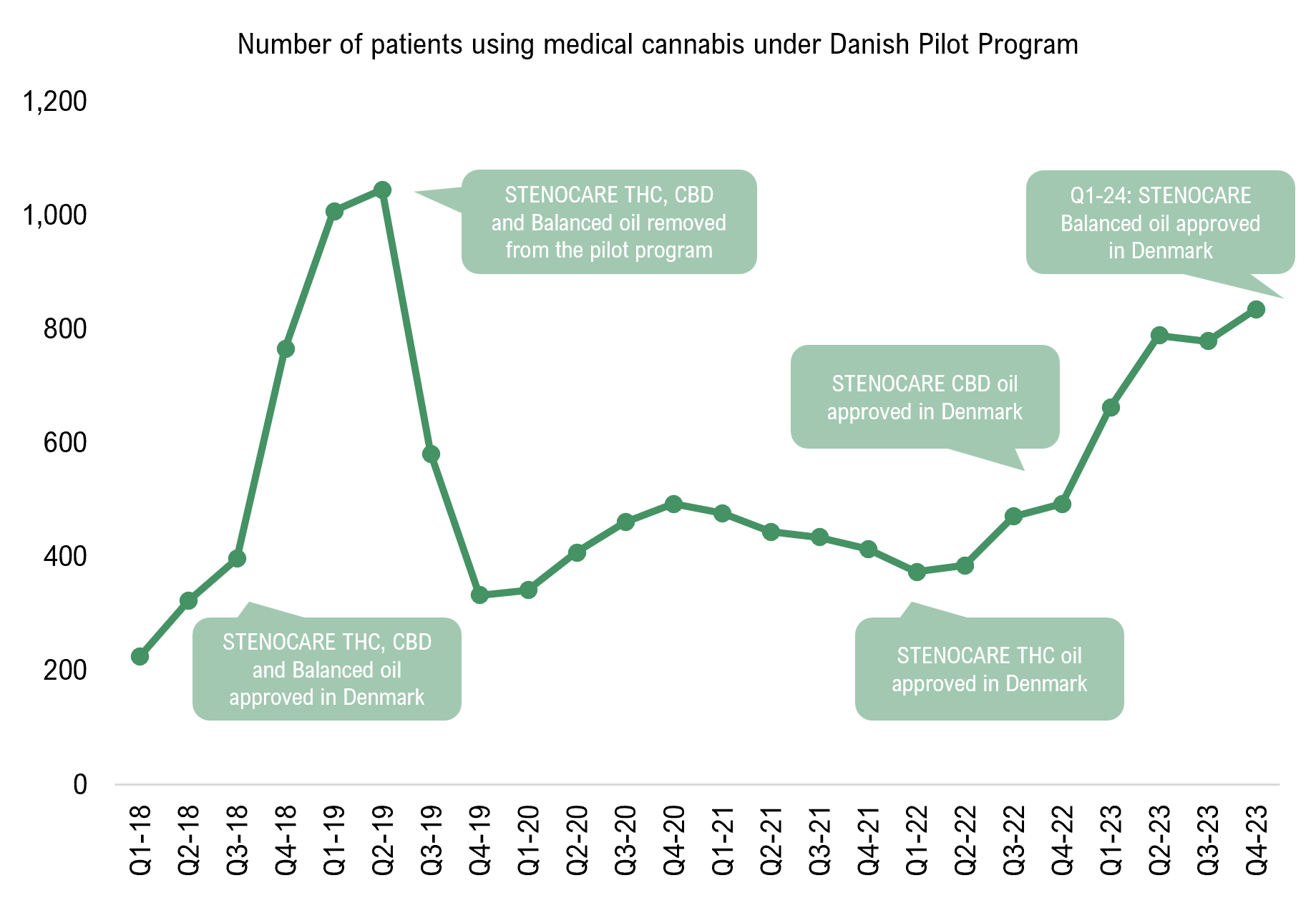

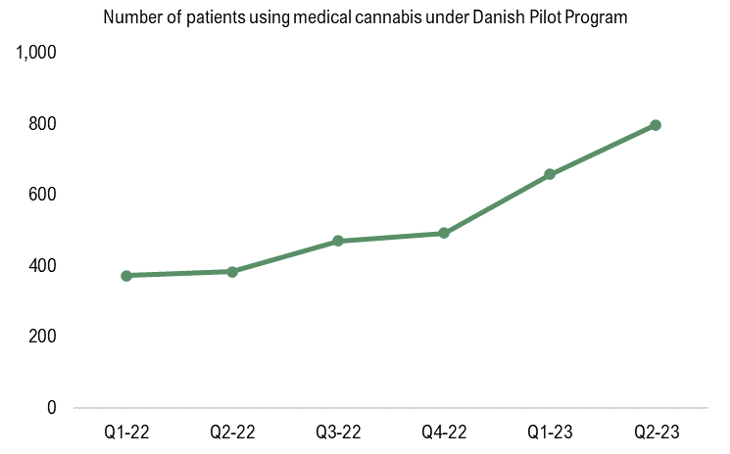

The number of patients using medical cannabis under the Danish pilot program had a stable development in Q1-24, which is the last published figures, amounting to 816 compared to 662 in Q1-23. When looking at the number of patients using medical cannabis under the Danish pilot program, the number of patients has historically increased after new products from STENOCARE has been approved as illustrated in the graph below. From April 18th, STENOCARE’s balanced oil has been approved for sales in Denmark, which historically has represented +50% of the total sales, why we estimate that the newly approved balanced oil will accelerate patient growth in the coming quarters, which is also expected to drive sales volume. However, due to price declines the total sales is expected to be lower than earlier anticipated in the coming quarters.

Capital Increases and Reduction of Debt but Additional Funding Expected to be Needed

During Q2-24, STENOCARE strengthened the cash position through warrants of series TO2 with net proceeds of approximately DKK 4.2m and a directed issue of DKK 1m to the major shareholder HHTM ApS. Moreover, STENOCARE negotiated a loan agreement with shareholder HHTM ApS amounting to DKK 2.8m with a slightly better interest rate than the existing debt (1.97% vs 2%) and with a loan term of 30 months compared to the existing debt of DKK 6m which was due on January 1st, 2025. Through the new loan, the directed issue and partial of the new proceeds from TO2 warrants, the existing debt of DKK 6m was repaid, leading to the total debt on STENOCARE’s balance sheet amounting DKK 2.8m after the transactions.

Through these activities, STENOCARE’s debt has decreased, and the cash position has strengthened, which we view positively. The transactions are not visible in the Q2-report as they were completed just after the end of the quarter. Given that the “old” debt of DKK 6m has been repaid with the new loan of DKK 2.8m, the proceeds from the directed issue of DKK 1m, we estimate that approximately DKK 2.2m of the proceeds from TO2 has been used to repay the loan, which leaves approximately DKK 2m as cash at bank at the end of Q2-24. The burn rate in Q2-24 was DKK -0.77m per month and given the financial performance in H1-24, the updated guidance, and the estimated cash balance of approximately DKK 2m at the end of Q2-24, Analyst Group believes that the company will need to secure additional funding, most likely through a capital raise.

To summarize, STENOCARE delivered a report with lower sales than estimated but also lower costs than expected. We continue to see several growth drivers, even though they are materializing more slowly than we previously anticipated, however we expect higher revenue in H2-24 compared to H1-24.

We will return with an updated equity research report of STENOCARE.

Comment on STENOCARE’s Q1-report Report 2024

2024-05-02

STENOCARE published on May 2 the company’s Q1-report for 2024. The following are some key points that we have chosen to highlight in connection with the report:

- Financial development during the period

- New product approved in Denmark

- Accelerated sales growth is important for the financial position

43% Sales Growth

STENOCARE’s net sales amounted to DKK 1.2m in Q1-24, corresponding to a growth of 43% compared to Q1-23 when net sales amounted to DKK 0.8m. The gross sales, excluding product returns, amounted to DKK 1.4m, corresponding to a growth of 62%. The sales in Q1-24 included delivery of products to the Danish market, where a new product was approved for sales in Q1-24, a mixed THC/CBD oil which historically has represented +50% of sales volume in the Danish market and expected to drive the sales growth in the coming quarters as the product is available for sale since April 2024. The new product is not included in the Q1 figures but sold to the distributors after the reporting period.

With reported sales of DKK 1.2m in Q1-24, STENOCARE has a way to go to reach our annual revenue forecast for 2024 of DKK 16.5m in a Base scenario. However, it should be noted that, as mentioned in our previous updates regarding STENOCARE, sales are expected to fluctuate between quarters as a result of the company delivering products in large bulks, which means that sales are affected by in which quarter larger deliveries occur. Given the approval of the balanced oil in Q1-24, we expect growing sales on the Danish market going forward, in combination with deliveries to international markets, where sales have so far developed slower than estimated. However, a new product was launched to the Australian market during Q1-24, which is expected to be a sales driver in that market moving forward. Moreover, STENOCARE entered the German market in Q4-23, where we expect more sales in the coming quarters.

Slightly Decreased Cost Base

The operational expenses, including depreciation, amounted to DKK -4.5m in Q1-24, compared to DKK -4.8m in Q1-23, corresponding to a decrease of 7%. Sequentially, the operational expenses decreased from DKK 5.1m in Q4-23, a reduction of 12%. The sales growth in combination with the decreasing cost base, the EBITDA result improved to DKK -2.5m in Q1-24 from DKK -3.2m in Q1-23. With a slim organization and lean cost base, the estimated accelerated sales growth is expected to lead to the anticipated break even by the end of 2024.

New Product Approved in Denmark

On February 26th, STENOCARE announced that a new product has been approved for sales under the Danish pilot program. The product is a mixed THC/CBD oil product, which means that STENOCARE has regained the position as the only provider of all three essential oil products under the Danish Pilot Programme: THC oil, CBD oil, and now also the new THC/CBD mixed oil. This means that STENOCARE are now back with three different products approved in Denmark, like in 2018/2019, before STENOCARE had to terminate the partnership with their then only supplier, CannTrust, and start to look for a new partner and again getting products approved by authorities, which has now been completed. When looking at the number of patients using medical cannabis under the Danish pilot program, the number of patients has historically increased after new products from STENOCARE has been approved as illustrated in the graph below. Moreover, in 2018/2019, the balanced oil represented +50% of the total sales, why we estimate that the newly approved balanced oil will accelerate patient growth in the coming quarters, thus also sales growth for STENOCARE.

Accelerated Sales Growth is Important for the Financial Position

The cash position at the end of Q1-24 amounted to DKK 2.6m, compared to DKK 9.5m at the end of Q4-23. In addition to the reported EBITDA loss, the cash position was affected by a repayment of convertible loans amounting to DKK 3.2m, which we accounted for in our comment on STENOCARE’s Q4 report. Based on the current cash position and an estimated burn rate of DKK -0.7m per month, STENOCARE would be financed until July 2024. However, the cash position can be strengthened in June by the exercise of warrants of series TO2, where 1,712,999 warrants can be exercised in the period 10 to 21 June 2024 with a price per share of the VWAP for the last 10 trading days before the exercise period beginning less 30%. Moreover, Analyst Group estimates, as previously mentioned, accelerated sales growth in the coming quarters to improve the cash flow, which we see as important to avoid further external capital raising in the future.

To summarize, STENOCARE delivered a stable report with a decreasing cost base. An accelerated sales growth is expected in the coming quarters, among other things through the introduction of new products in Denmark as well as Australia to reach our sales forecast of DKK 16.5m for 2024, which is also important for the cash position to avoid further external capital raising in the future.

We will return with an updated equity research report of STENOCARE.

Comment on STENOCARE Expanding in Australia

2023-12-14

STENOCARE announced on December 14th that the company has entered into a new partnership agreement with Quest Biotech Pharma (“QBP”), aimed at expanding its reach to more prescribing doctors and patients in Australia.

New Partnership to Increase Doctors Reach

QBP is a highly specialized Australian pharmaceutical company who can increase the capacity of prescribing doctors of STENOCARE branded products via multiple channels. QBP has a pharmaceutical approach to medical cannabis education and offers free and balanced educational resources on medical cannabis to patients, nurses, doctors, and pharmacists. For instance, QBP partners with a holistic tele healthcare clinic – TeleDocs Clinic – serving patients with convenient access to medical care services nationwide. This is expected to increase prescribing doctors reach to patients, just like STENOCARE’s own online clinic, as TeleDocs Clinic addresses all of Australia. The agreement has the potential to double the sales run rate of STENOCARE-branded products in Australia during 2024.

Analyst Group’s View of the Partnership

In our last equity research reports we have stated the importance of ensuring the health care industry’s interest and thus that doctors are willing to prescribe medical cannabis to patients. An essential step for this to happen is to educate doctors about the benefits of medical cannabis and the treatment process, as there are significant knowledge gaps in the market today. The partnership with QBP is expected to address this issue since the QBP pharmacists provide free and balanced education about medicinal cannabis to patients, nurses, doctors, and pharmacists. Consequently, more doctors can be educated about the advantages of medical cannabis and, in turn, prescribe it. Additionally, STENOCARE’s dosing method is expected to be advantageous in persuading doctors to prescribe medical cannabis, as they are accustomed to dosing with oils in other medications, compared to other products such as dried cannabis, which is used for smoking and is generally perceived as more harmful.

Furthermore, the partnership with QBP is expected to enable doctors prescribing STENOCARE’s products to expand their reach to patients, given QBP’s partnership with the holistic telehealth clinic, TeleDocs Clinic. Just like with STENOCARE’s own online clinic, doctors, with the assistance of TeleDocs Clinic, can reach patients across the entire country, thereby increasing the number of addressable patients. Given that Australia is a vast and sparsely populated country, it is crucial to be able to reach extensive areas to address as many patients as possible, making a tele healthcare clinic a suitable solution.

In summary, Analyst Group views positively on STENOCARE’s new partnership with QBP, as we anticipate that it will result in an increased number of prescriptions by doctors in Australia, contributing to strong revenue growth in the country in the coming years and beyond.

How Analyst Group sees STENOCARE as an investment

The number of patients continued to grow strongly during Q3-23 for STENOCARE A/S (“STENOCARE” or “the Company”) which resulted in actual sales of DKK 2.3m. The reported net sales amounted to DKK 0.2m but included a large product return from Norway of DKK 2.1m, which we consider as a one-of occasion. Adjusted for the product return, EBITDA amounted to DKK -1.7m, the best in a quarter since Q1-19 and we estimate STENOCARE to reach break-even by the end of 2024. With estimated net sales of DKK 66.6m by 2026, and with an applied P/S multiple of 5x, a potential present value per share of DKK 9.4 (10.2) is derived in a Base scenario.

Comment on STENOCARE Adding a new Product in Australia

2023-11-23

STENOCARE announced on November 23rd that the company has signed agreements that will make a new product, a Balanced 25-25 oil, available for patients in Australia from Q1-24. The decision comes after sales in the country have performed better than budgeted.

Adding a new Product is seen as a Natural Step

STENOCARE entered Australia in 2022 with the Balanced 12.5-12.5 oil and the response from doctors and patients has exceeded the expectations. As a result, STENOCARE is now launching a new product in the country, a Balanced 25-25 oil, hence providing choices for both first-time medical cannabis users and experienced patients, which will expand the reach to doctors and patients. Typically, when patients start medication with medical cannabis, a lower dose is needed to avoid more significant side effects. Therefore, STENOCARE began by introducing the slightly weaker 12.5-12.5 oil. However, as patients become accustomed to the dosage, and symptoms evolve, it may be relevant to increase the dosage. Consequently, STENOCARE is now launching the balanced 25-25 oil. The launch is seen as a natural step to continue treating patients who need to progress to a stronger dosage, thus preventing the loss of these patients to competitors.

Market with Large Potential