STENOCARE published on June 20 its Q1-report for 2023. The following are some key points that we have chosen to highlight in connection with the report:

- Financial development during the period

- Unit Rights Issue has strengthened the financial position

- One of STENOCARE’s competitors are closing the factory in Denmark

Financial Development During the Period

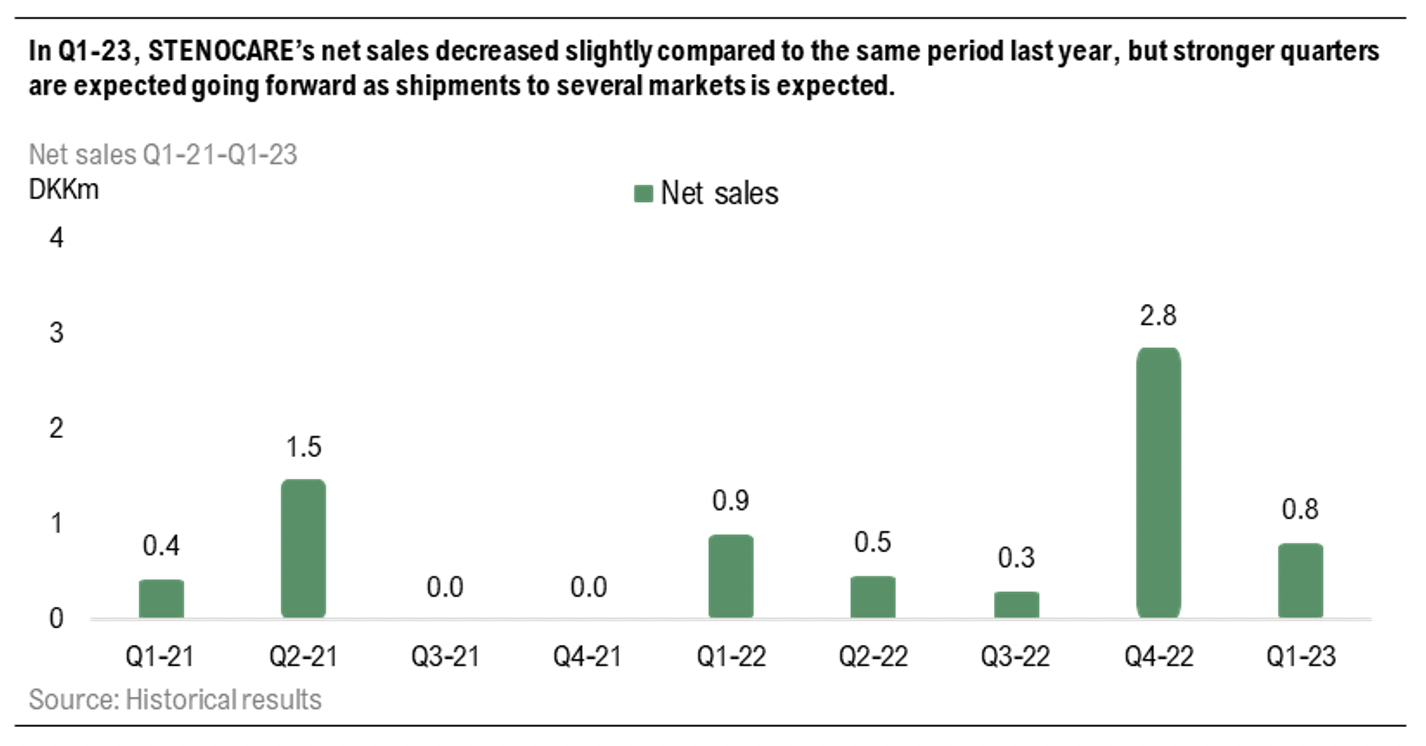

STENOCARE’s net sales during Q1-23 amounted to DKK 0.8m, compared to DKK 0.9m during Q1-22 and DKK 2.8m during the last quarter (Q4-22). The sales during Q1-23 consists of products sold in Denmark, which is one of STENOCARE’s now six markets. As we have emphasised in previous comments and equity research reports, sales are expected to fluctuate from quarter to quarter as a result of orders being shipped in large quantities, because of distribution partners wanting to reduce their logistical costs. This is expected to be a competitive advantage going forward but can, as earlier mentioned, result in a fluctuation in sales from quarter to quarter. Hence, as STENOCARE delivered products to five countries during Q4-22 and the first shipment to Norway was completed at the end of December 2022, a lower activity regarding delivering products could be expected during Q1-23. However, we expect stronger quarters ahead regarding sales, as products are delivered to several markets and the company is entering Germany, where products are expected to be available for patients in August 2023.

The cost development was stable during Q1-23, as external expenses amounted to DKK 2.5m compared to DKK 2.7m during Q1-22 and personnel expenses amounted to DKK 1.5m, compared to DKK 1.6m during Q1-22. The decrease in costs shows that STENOCARE is still running a slim organization towards the expected break-even by Q4-23. The lower costs resulted in a slightly better EBITDA-result, amounting to DKK -3.2m, compared to DKK -3.4m during Q1-22. Regarding cash flow, the cash flow from operating activities amounted to DKK -2.3m and the cash position amounted to DKK 1.9m. However, STENOCARE has received DKK 10.7m in gross proceeds from a Unit Rights Issue during June 2023, with warrants of series TO 1 and TO 2 that can add gross proceeds of DKK 3.7-7.8m and DKK 3.7-11.2m in December 2023 and June 2024 respectively.

STENOCARE’s Rights Issue was Subscribed to approximately 127%

The Unit Rights Issue during May and June 2023 was subscribed to approximately 127%, which implies a big interest in STENOCARE as an investment. The gross proceeds from the Issue will be used to further scale the core business, which includes obtaining approval for new products as well as commercial efforts in current and new markets, investment in the completion and commercialization of STENOCARE’s own indoor cultivation facility, and repayment of short-term debt. The Rights Issue is expected to allow STENOCARE to accelerate commercial activities, hence scale up sales and strengthen the company’s financial position. For more information on our view on the Rights Issue, we refer to our previous comment here. Moreover, a conversion of short-term debt of DKK 3.1m into shares in a separate parallel directed issue on identical terms with the Initial Rights Issue is expected, which further strengthens STENOCARE’s financial position. The fact that loan givers have committed to a conversion of debt to shares shows that loan givers believe in STENOCARE’s strategy and ability to create shareholder value going forward.

Denmark’s Largest Cannabis Factory is Closing – Proof of STENOCARE’s Strategy

Canadian cannabis supplier Aurora Cannabis started Aurora Nordic in 2018, with the aim to cultivate and sell medical cannabis to Danish as well as European patients. Since the start, Aurora Nordic have made investments amounting to approx. DKK 500m in their cultivation facility and is currently the largest exporter of medical cannabis in Denmark. However, Aurora have met challenges regarding getting products approved, especially under the Danish pilot program, as only one product has been approved in Denmark since 2018, proving the difficulty to manage the regulation. A possible explanation to this according to Analyst Group, as we have stated in our previous equity research reports, could be that Aurora grows its medical cannabis in greenhouses, unlike STENOCARE’s indoor cultivation, a method that may complicate compliance with regulatory agencies, particularly those concerning the use of pesticides. The Canadian owner Aurora Cannabis have now decided to close its cultivation facility as the profitability of the cultivation facility has not reached expectations, as a result of the facilities large capacity compared to what has actually been sold. This proves, according to Analyst Group, that STENOCARE’s strategy with indoor cultivation and have a supply chain that can grow volume when demand increases, is better for a sustainable business model.

Several Highlights After the Period – STENOCARE Enters Germany

On May 25th, STENOCARE announced that a new medical cannabis oil product has received approval for sales in Germany, which is the 6th country with products approved from STENOCARE. The German market for medical cannabis is by far the largest in Europe, with over 200,000 patients being treated with projected sales of EUR 1bn by 2027. This can be compared to the entire European market, where the total sales are expected to reach sales of EUR 2.2bn by 2027, thus the German market is expected to stand for almost half of the total sales on the European market, showcasing the potential of the market. To read more about our view of STENOCARE entering Germany, read our comment here.

Moreover, STENOCARE announced on May 30th that the company has developed an IT-platform that enables doctors to launch and operate Online Clinics, which is expected to increase a doctor’s reach to patients across their geography and facilitates patients’ access to trained and experienced doctors and specialists. Read our comment on the news here. Lastly, STENOCARE has also announced that the company has selected a partner to produce its premium products, which are based on patented oil technology. The oil technology enables, according to studies, better uptake of cannabinoids, regardless of meal consumption and inter-individual biological differences, as well as a faster effect. A common challenge for doctors within medical cannabis is the accuracy of the dosage uptake for the patients, as this varies depending on whether the drug is taken before or after intake of food and individual biological differences, why a more predictable product like STENOCARE’s premium products is expected to be appreciated by doctors. The company announced that the products are likely to become commercially available during 2024, which is in line with what we have expected in our financial forecasts in previous equity research report updates.

To summarize, STENOCARE delivered a slight decrease in net sales during Q1-23 but where a slower quarter regarding net sales could be expected as large quantities of products were delivered at the end of Q4-22 and sales are expected to fluctuate from quarter to quarter depending on which period a large delivery is made. Hence, we expect stronger sales growth in the coming quarters, together with a continued stable cost base. Furthermore, we see proof on the market that STENOCARE’s strategy is working, as competitor Aurora Nordic have had troubles getting products approved and are closing the factory in Denmark at the same time as STENOCARE is entering new markets, showing that the company’s pharma mindset is paying off.

We will Return with an Updated Equity Research Report of STENOCARE.