Movinn published on May 4th the companys Q1-report for 2023. The following are some key points that we have chosen to highlight in connection with the report:

- Revenues slightly above our estimates

- Higher costs than expected – but better efficiency is expected going forward

- Positive signs in the cash flow statement – better cash flow expected in the coming quarters

Revenues slightly above our estimates

Movinn’s revenue amounted to DKK 20.6m during the first quarters, close in line with our estimates of DKK 20.2m. The revenue growth amounted to 27% compared to the same period last year, when the revenue amounted to DKK 16.2m. The revenue growth compared to last year is a result of Movinn’s strong unit growth during 2022, which is now materializing in sales. Furthermore, the revenue per unit amounted to DKK 198t on the Danish units and DKK 83t on the Swedish units, which can be compared to DKK 183t and DKK 20t respectively for the full year 2022. Analyst Group estimates the revenue per unit on the Danish units to DKK 192t and for the Swedish units to DKK 90t for the full year 2023. As we expect the revenue per unit to increase successively over the year because of new units maturing, we believe that the first quarter results regarding revenue per unit were strong and above what we expected. The strong revenue per unit was achieved despite the higher-than-expected vacancy rates of 16.1% on the Danish units and 27.9% on the Swedish units, why we estimate the revenue per unit to increase even further when demand improves, and vacancy rates decreases to more normal levels. Demand is expected to improve in the coming quarters due to the natural seasonal pattern where the second and third quarters are usually stronger for Movinn, as well as through a well-diversified client portfolio.

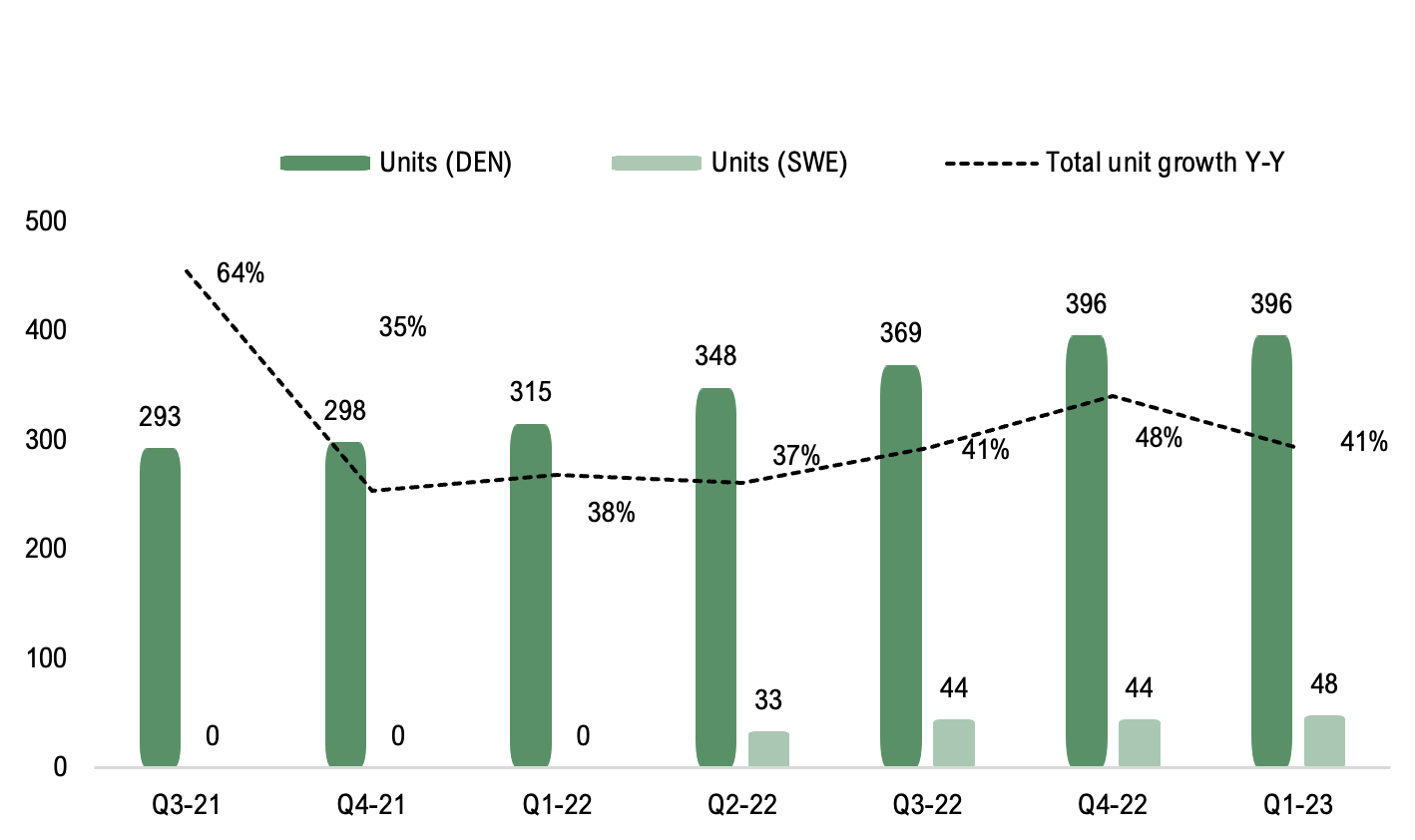

Regarding unit growth, Movinn grew its unit portfolio by four new units during the first quarter, which were added on the Swedish market. A slower unit growth was expected as the company focuses on fully integrating units that was added during 2022, hence increasing bottom line performance and cash flows. Furthermore, Movinn is currently going through a change in strategy, taking on larger projects, i.e., projects with more units at once, meaning more units will be added at the same time compared to several smaller units in different locations as has been the case in the past. This strategy is expected to lead to lower costs going forward, as larger contracts are easier to negotiate and maintenance of units in the same building is more efficient, but also that unit growth will fluctuate more between quarters. Moreover, Collective yoyo, Movinn’s brand for furniture rental was launched during the quarter. Even if the brand is new and stands for a minor part of the revenue share (1%), we see positive on this as it adds an additional revenue stream for the company, as well as activating the furniture on the balance sheet. Analyst Group estimates that Collective yoyo will increase its revenue share going forward.

Higher costs than expected – but better efficiency is expected going forward

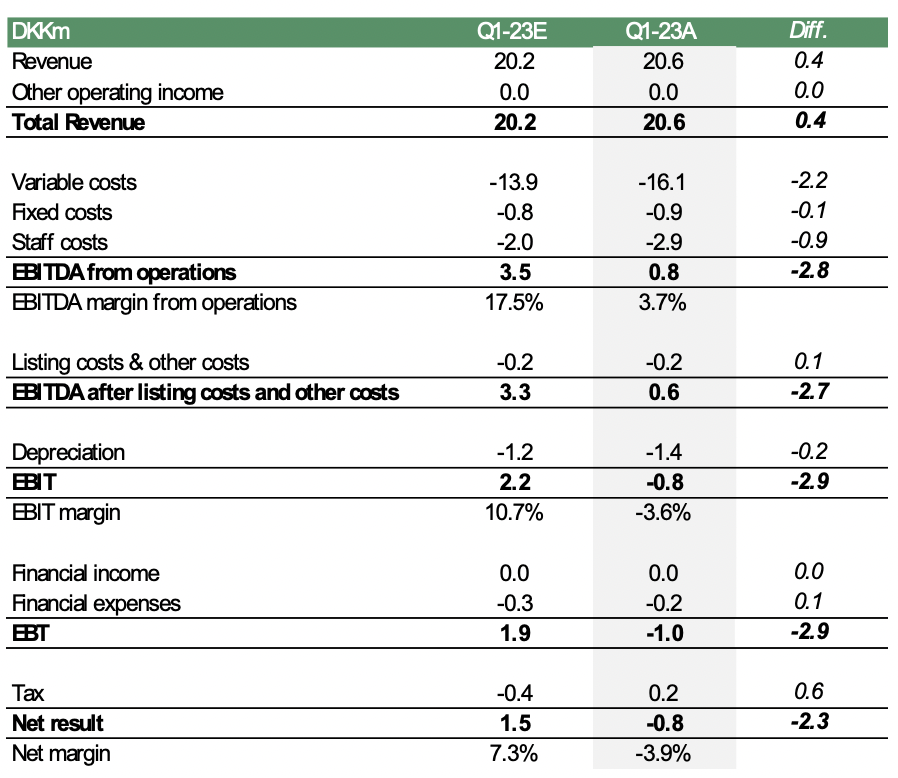

The variable costs in Q1-23 amounted to DKK 16.1m, which was higher compared to our estimates (13.9) and the same period last year (11.9). The higher costs are a result of changes in the organization and processes to sustain future growth. However, Analyst Group expects the variable costs to decrease in relation to revenues going forward, primarily driven by the company taking on larger projects going forward, leading to a better negotiation position as well as better efficiency in maintenance. Furthermore, Analyst Group expects that macroeconomic factors, such as continued decreased inflation and energy prices, will decrease Movinn’s cost base going forward. On a positive note, the Swedish subsidiary is approaching break-even and is expected to contribute with a positive EBITDA from operations at the end of the year. EBITDA from operations amounted to DKK 0.8m for the first quarter, compared to our estimates of DKK 3.5m. The table below shows a complete comparison between our estimates and the result.

Positive signs in the cash flow statement – better cash flow expected in the coming quarters

The cash flow from operating activities amounted to DKK -0.8m, compared to DKK 0.4m during the same period last year, where the decrease is attributable to the higher costs during Q1-23. However, regarding the cash flow from investing activities, we can see a decrease in investments in fixed assets as well as security deposits, which is assumed to be due to fewer units being added. Going forward, as costs are expected to decrease, hence contributing to an increased EBIT, we expect a positive effect on the cash flow going forward through the decreasing investments. Furthermore, when entering the German market, which is expected in 2024, Movinn is expected to replace security deposits with rental guarantees, which is expected to decrease investments further, hence contributing to improved ROIC and cash flow.

To summarize, Movinn delivered a first quarter with slightly higher revenue than expected, where a strong revenue per unit was the largest contributor, despite a higher-than-expected vacancy rate. Going forward, when demand is expected to improve and vacancy rates drop, we estimate that this will result in a higher revenue per unit. Regarding costs, the variable costs and staff costs were higher than expected, but where we see improvement going forward as the macroeconomic situation improves, as well as the company taking on larger projects.

We will return with an updated equity research report of Movinn.